Only relying on code, without the involvement of banks, governments, or other centralized entities, DeFi (Decentralized Finance) can automatically execute trades, loans, and transfers. It is a financial system built on blockchain and smart contracts that enables transactions, borrowing, and payments without the need for traditional intermediaries.

Many trend reports forecast that DeFi will be a major focus in 2025, as people become increasingly conscious of “financial sovereignty.” VanEck, one of the world’s largest ETF managers, predicts that more capital will flow into DeFi by 2025, with decentralized exchange (DEX) trading volume potentially surpassing four trillion USD. The total value locked (TVL) in DeFi platform smart contracts could also break 200 billion USD by the end of 2025.

What exactly is DeFi? Why should you pay attention to it? What potential does it hold for the future? Let’s break it down.

From three major dimensions—technology, regulation, and application—we systematically outline DeFi’s core concepts and operating mechanisms, and we deeply assess its advantages and risks. Through case analysis, readers can grasp the potential opportunities and challenges of decentralized finance and gain a panoramic view of the future shape of finance.

What Is DeFi?

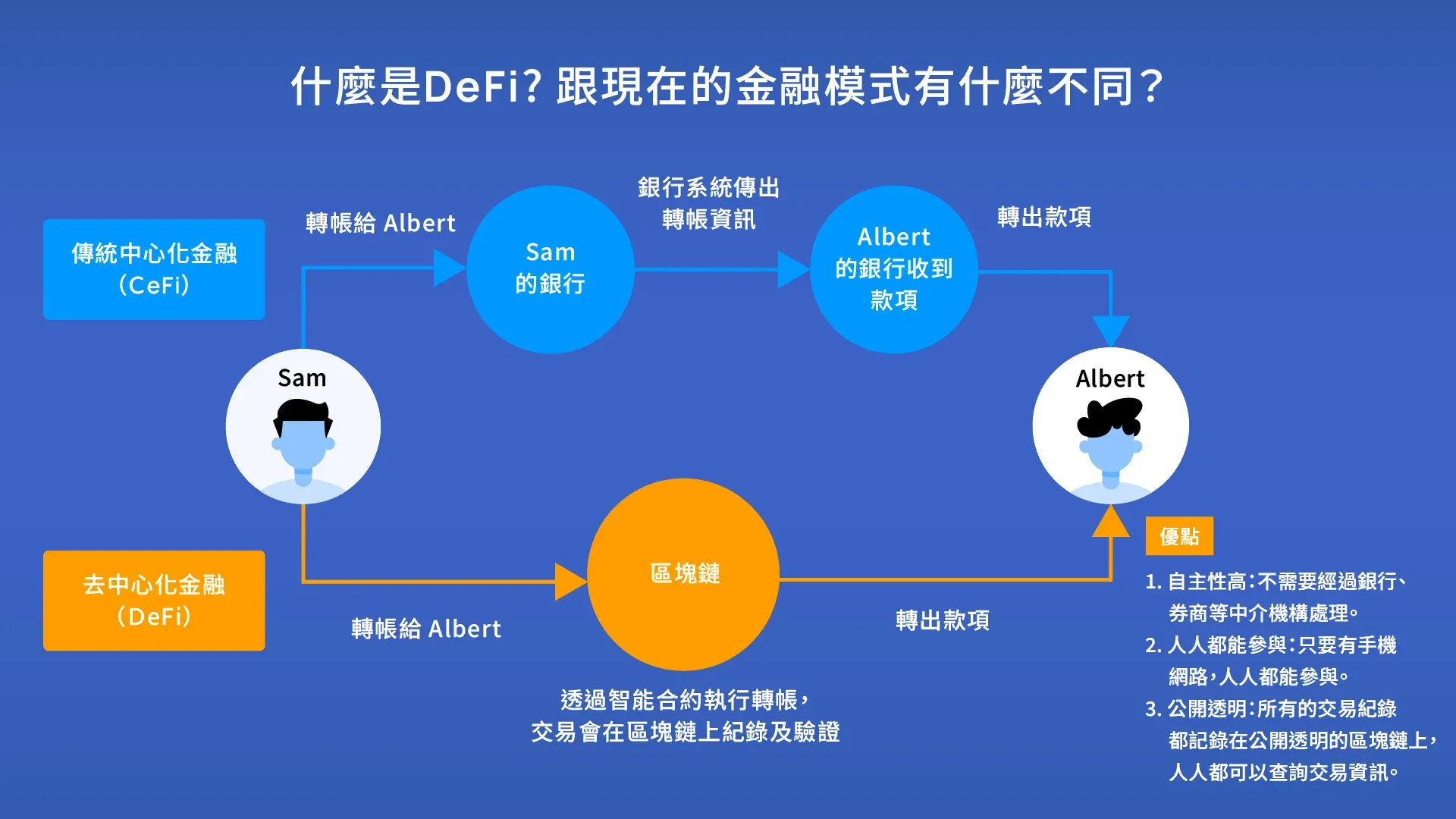

DeFi (Decentralized Finance) refers to a financial system built on blockchain technology that operates through smart contracts.

Definition: A smart contract is a set of contractual terms written as code and stored on the blockchain; once the trigger conditions are met, it executes automatically without the need for banks, lawyers, accountants, or any other centralized authority.

The core characteristic of DeFi is that transactions, transfers, and lending can be completed solely via code, with no traditional intermediaries involved. All operations are transparent, publicly auditable, and automatically enforced, allowing anyone to participate.

Advantages of DeFi

- High autonomy: Smart contracts execute automatically, eliminating banks, brokers, and other middlemen, which reduces transaction costs.

- No bank account required: With just a smartphone and internet connection, anyone can access DeFi without undergoing account opening, credit checks, or proof‑of‑funds procedures.

- Public transparency: Blockchain records are available 24/7 worldwide. According to World Bank data, transaction records for roughly 1.4 billion people have already been on‑chain and are accessible to anyone.

Disadvantages of DeFi

- High entry barrier: The lack of a single operating authority means users must manage their own wallets and sign contracts themselves, demanding a certain level of technical competence; novices can easily incur losses through mistakes.

- Significant security risk: If a smart contract contains bugs or is hacked, assets may be lost in large sums. The decentralized nature also means there is no customer‑service support, making recovery of lost funds extremely difficult.

Understanding DeFi’s Three‑Phase Evolution: From the “DeFi Summer” to the 3.0 Era

Since the birth of smart‑contract technology in 2015, DeFi has been evolving for about a decade and can be divided into three primary stages.

2020: The “DeFi Summer”

The year 2020 is dubbed the “DeFi Summer,” marking the first large‑scale public exposure of DeFi. The pandemic and ensuing economic crisis sparked a flight‑to‑safety mindset, while USD liquidity tightened. Three key factors together fueled DeFi’s breakout:

- Maturity of Ethereum: Provided a solid foundation for smart contracts.

- Shortcomings of traditional finance: Drove demand for more efficient, transparent, and open financial services.

- Continued venture‑capital inflows: Sustained funding for DeFi projects.

A flagship example was the decentralized lending platform Compound Finance, which launched its governance token COMP and ignited the “liquidity mining” craze. Liquidity mining works by having users deposit two crypto assets into a liquidity pool; the platform charges transaction fees and rewards a portion of those fees to liquidity providers. This mechanism attracted massive capital, pushing DeFi’s TVL from $700 million at the start of 2020 to roughly $15 billion by year‑end.

Tax note: In many jurisdictions, profits generated from liquidity mining or other DeFi activities may be subject to capital‑gains tax. Participants should consult local tax regulations.

2022: DeFi 2.0

The rapid expansion of DeFi 1.0 exposed problems such as over‑incentivization and uneven distribution of governance tokens. DeFi 2.0 introduced new concepts aimed at improving efficiency, sustainability, and security:

- Protocol‑Owned Liquidity (POL): Protocols issue and manage their own native tokens to provide liquidity, reducing dependence on external capital.

- More sophisticated token‑economics designs intended to balance incentives against risk.

Representative projects include:

| Project | Core Innovation |

|---|---|

| Olympus DAO | Decentralized reserve currency that builds a self‑regulating asset pool |

| Aave V4 | Next‑generation lending protocol that enhances capital efficiency |

| Hyperliquid | Decentralized perpetual futures exchange |

| Uniswap v4 | Introduces custom aggregators to increase trading flexibility |

These innovations laid a new foundation for DeFi’s sustainable growth.

2025: DeFi 3.0

Entering the 3.0 era, DeFi begins to break out of the purely crypto‑trading niche and deeply integrates with real‑world assets (RWA), while also attracting traditional institutions.

- RWA Integration: Platforms like Propbase tokenize real‑estate assets, enabling borrowing and trading, thereby improving liquidity and lowering entry barriers for investors.

- Institution‑Grade DeFi: Traditional asset‑management firm Franklin Templeton launched Benji Investments on Polygon, offering institutional investors a gateway to DeFi yield products.

- Security and UX upgrades: Multi‑layer protections, formal verification, and AI‑driven security systems are becoming mainstream; Ethereum’s Account Abstraction and Social Recovery Wallets reduce the risk of private‑key loss and improve user friendliness.

Balancing Centralization and Decentralization – The Dawn of a New DeFi Era

Although DeFi is only a decade old, its user base has grown from under 500 k in 2020 to over 10 million today. Winston Xiao, co‑founder and revenue chief of XREX, notes that as global regulatory frameworks mature, centralized finance will become more standardized, making 2025 a watershed year between “centralized” and “decentralized” models. Clearer regulations will boost the reliability of centralized services while simultaneously highlighting the demand for decentralized alternatives.

This year, Taiwan’s Financial Supervisory Commission upgraded the virtual‑asset service provider (VASP) regime from a registration‑based to a licensing‑based system, gradually moving toward a permit‑only model that limits the number of approved operators. This trend could create an imbalance between centralized and decentralized services, but it also opens up additional room for DeFi expansion.

DeFi 3.0 is not only reaching technical maturity; its application landscape is expanding dramatically. The active participation of traditional institutions, deep coupling with the real economy, and a proactive stance toward regulation position DeFi as a key engine of financial innovation, expected to exert a profound influence on the global financial architecture.

---

That concludes the article “What Is DeFi? Decentralized Finance – Advantages, Disadvantages, and Future Potential.” For a more comprehensive overview of DeFi, search for previous Bitaigen (比特根) articles or continue browsing the related links below. Thank you for supporting Bitaigen (比特根)!

Related Reading

- DeFi Explained: Decentralized Finance Transforming Banking

- Understanding Blockchain IDOs: A Simple Guide Compared to IPOs and ICOs

- DeFi Liquidity Mining: Unlock 100x Token Potential

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.