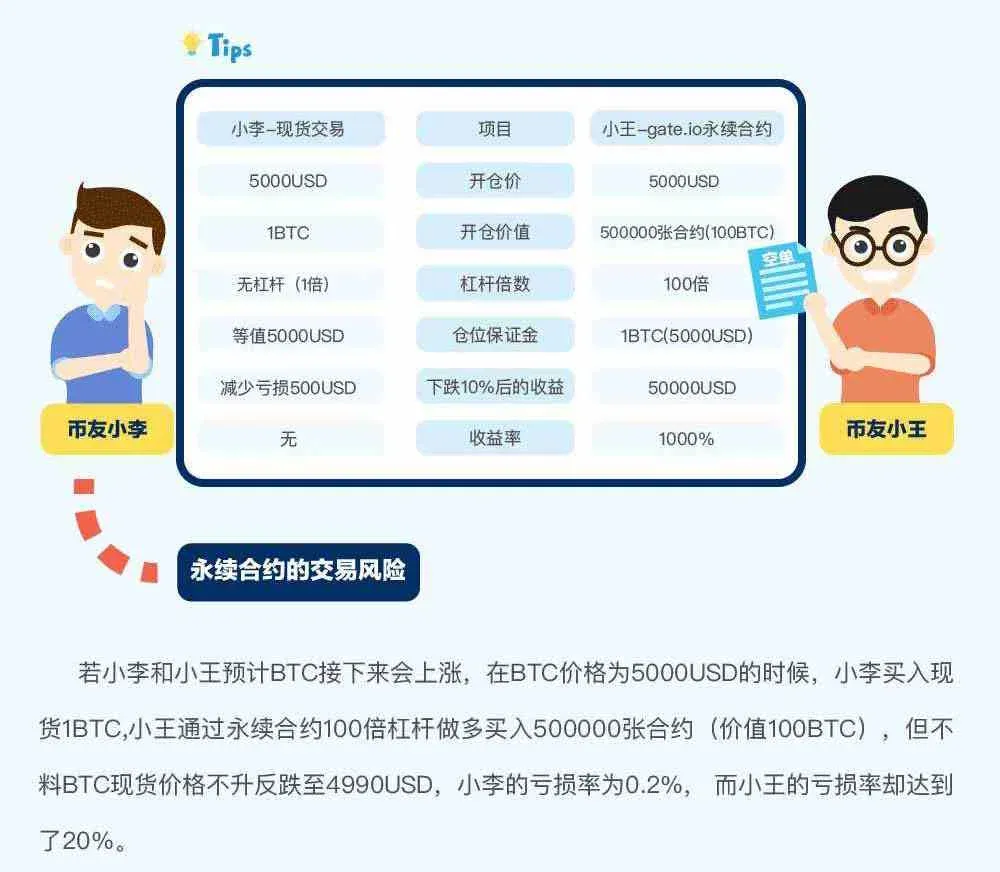

We systematically outline the core trading rules for gate.io perpetual contracts in this article, covering fee structures, contract categories, margin requirements, and liquidation mechanisms. The aim is to help beginners get up to speed quickly while providing detailed references for experienced traders. Subsequent sections will expand on each point, so please continue reading.

Detailed Rules for Perpetual Contract Trading on the gate.io Platform

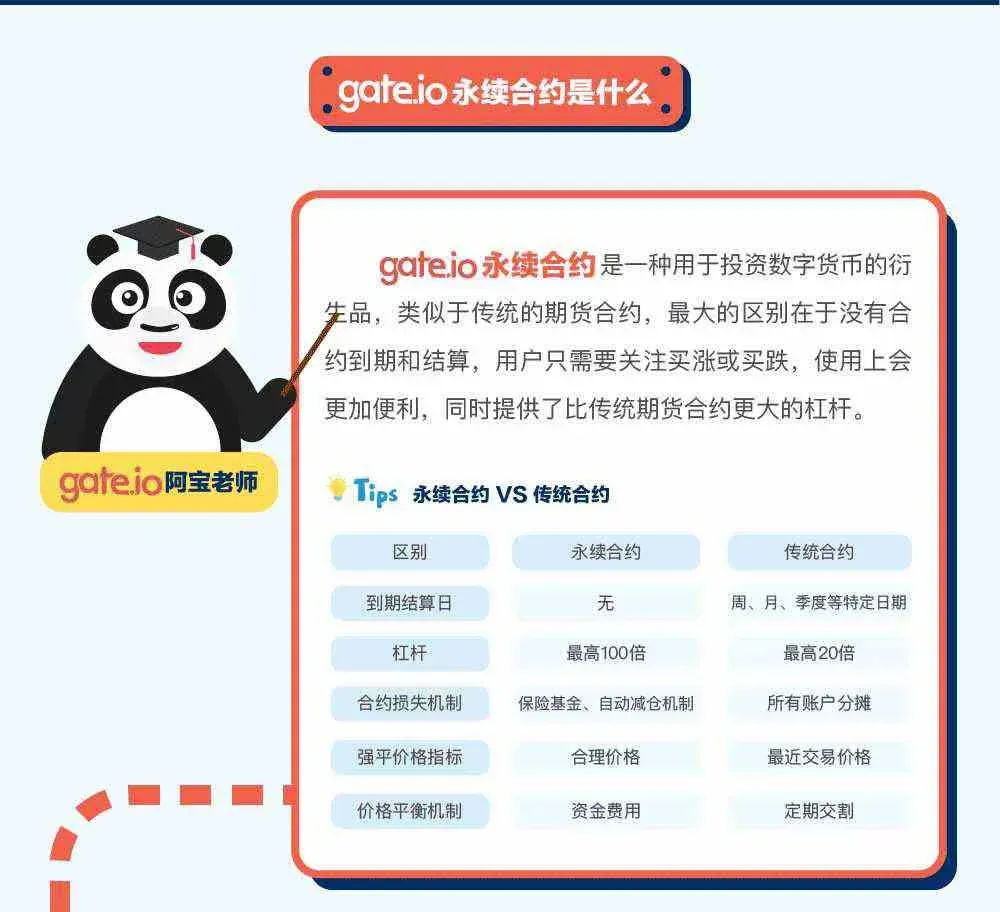

gate.io perpetual contracts are crypto‑financial derivatives with no expiry date and the ability to hold positions indefinitely. Their trading rules encompass fees, contract types, margin, and forced liquidation.

What Is a Perpetual Contract

A perpetual contract is a financial derivative linked to a digital asset. Unlike traditional futures, it has no settlement date, allowing users to keep a position open for as long as they wish. This design makes the trading experience resemble spot trading more closely.

---

Perpetual Contract Fees

gate.io differentiates fees for perpetual contracts between Maker (limit orders) and Taker (market‑order execution). Makers can even receive a fee rebate.

| Contract | Maker Fee | Taker Fee |

|---|---|---|

| BTC/USD Perpetual | **‑0.025 %** (rebate) | **0.075 %** |

Fees are calculated on the notional value of the position and are independent of the leverage multiplier.

---

Contract Types and Currency Concepts

- Base currency: The underlying asset being traded, e.g., BTC, ETH.

- Quote currency: The currency used to quote the price, e.g., USD, USDT.

- Settlement currency: The actual token used for settlement in the user’s wallet. gate.io standardizes this to BTC.

Based on the combination of these three currencies, perpetual contracts fall into three categories:

- Standard Linear Contract

- Quote currency and settlement currency are the same.

- Example: EOS/BTC (base = EOS, quote / settlement = BTC).

- The price is expressed as “1 EOS equals how many BTC,” which is the closest representation to spot trading.

- Quanto Contract (Dual‑Currency)

- Quote currency differs from settlement currency.

- Example: ETH/USD (base = ETH, quote = USD, settlement = BTC).

- Suitable for traders who prefer a fiat‑denominated quote but do not wish to hold the base asset in their wallet.

- Inverse Contract

- Base currency and settlement currency are identical.

- Example: BTC/USD (already available).

- The price is quoted in USD while the entire trade—including margin and profit‑loss settlement—is conducted in BTC.

---

Value and Profit‑Loss Calculations

The formulas for determining contract value and profit/loss differ by contract type:

| Contract Type | Value Calculation | P/L Calculation |

|---|---|---|

| Standard Linear | Position Size × Price | Position Size × (Exit Price ‑ Entry Price) |

| Quanto | Position Size × Price × **Conversion Factor** | Position Size × (Exit Price ‑ Entry Price) × Conversion Factor |

| Inverse | Position Size ÷ Price | Position Size × (1 / Entry Price ‑ 1 / Exit Price) |

---

Why the Quote Currency Is USD Instead of USDT

USDT is a stablecoin often used in spot markets to bridge crypto and fiat values. In perpetual contracts, only one settlement currency is needed to settle trades and P/L. Using USD eliminates the risk that fluctuations in the USDT‑USD peg could affect contract valuation.

---

Long and Short Directions

- Long (Buy): Anticipate a price rise; profit if the price climbs after entry, otherwise incur a loss.

- Short (Sell): Anticipate a price decline; profit if the price falls after entry, otherwise incur a loss.

For any given contract, an account may hold only one directional position at a time—it cannot be both long and short simultaneously.

---

Leverage and Margin

Initial Margin

The minimum margin required to open a position. Calculations:

- Order Initial Margin = (Order Notional ÷ Leverage) + Opening Fee + Closing Fee

- Position Initial Margin = (Position Notional ÷ Leverage) + Closing Fee

Maintenance Margin

The minimum margin needed to keep an existing position alive:

- Position Maintenance Margin = (Position Notional × Maintenance‑Margin Ratio) + Closing Fee

The maintenance‑margin ratio is typically half of the inverse of the maximum leverage. For example, a maximum leverage of 100× corresponds to a maintenance‑margin ratio of 0.5 %.

Forced Liquidation

If the margin balance (including unrealized P/L) falls below the maintenance‑margin level, the system triggers a forced liquidation. The liquidation price is the Mark Price at the moment of trigger, and the liquidation process proceeds through the market, the insurance fund, and finally an automatic reduction system.

---

Mark Price

gate.io calculates the Mark Price by taking a weighted average of external market prices and adding a time‑decaying funding‑rate basis. This price is used to decide whether a liquidation should occur. The purpose of the Mark Price is to:

- Prevent malicious manipulation of the intra‑exchange price that could cause unnecessary liquidations.

- Anchor the exchange’s internal price to external spot prices, reducing the risk of price divergence.

---

Insurance Fund and Automatic Reduction System

- Insurance Fund: When a liquidation occurs at a price better than the bankruptcy price, any surplus is transferred to the insurance fund. The fund is then used to absorb future liquidation orders.

- Automatic Reduction System: If the insurance fund is still insufficient to cover a liquidation, the system automatically reduces positions of users holding profitable inverse contracts. Those users have their open orders canceled first, and the reduction proceeds from the highest‑earning accounts.

gate.io displays an “automatic reduction ranking” indicator on its interface; the more lights a user has, the higher the rank and the greater the likelihood of being selected for reduction. Users can lower this risk by manually closing positions and reopening them later.

---

Isolated Margin vs. Cross Margin

| Mode | Source of Margin | Risk Characteristics |

|---|---|---|

| **Isolated** | Separate margin allocated to each position (initial margin) | If the margin balance drops below the maintenance level, that specific position is liquidated. Losses are limited to the margin allocated to that position. |

| **Cross** | The entire available account balance acts as a unified margin pool | Multiple positions share the same margin pool, allowing profits and losses to offset each other. However, unrealized P/L cannot be used as margin for other positions. |

---

Funding Fee

Funding fees keep the perpetual contract price aligned with the underlying spot price. Calculation:

- Funding Fee = Position Value × Funding Rate

- When the funding rate is positive, longs pay shorts; when negative, shorts pay longs.

Funding fees are settled every 8 hours (UTC 00:00, 08:00, 16:00). The rate is determined by the interest‑rate differential between the quote and settlement currencies and the basis between the intra‑exchange and external prices.

---

Order Types and Practical Tips

| Order Type | Main Characteristics |

|---|---|

| **Standard Order** | Attempts to take liquidity first; any unfilled portion becomes a limit order. |

| **Immediate‑Or‑Cancel (IOC)** | Only takes liquidity; any unfilled portion is cancelled instantly (commonly used for market orders). |

| **Passive Order** | Places only limit orders without taking liquidity, avoiding Taker fees. |

| **Reduce‑Only Order** | Executes solely to close existing positions; any amount exceeding the current position size is cancelled. |

| **Close‑Only Order** | Each position can have only one close‑only order, which also has the reduce‑only property. |

| **Iceberg Order** | Shows only a portion of the total quantity; the hidden portion is revealed as the visible part is filled. Filled amounts are charged at the Taker fee rate. |

| **Strategy Order** | Automatically places an order when predefined trigger conditions are met. |

| **Take‑Profit/Stop‑Loss Order** | A subset of strategy orders; after the trigger, the system validates the order before converting it into an actual executable order. |

If a take‑profit/stop‑loss order triggers and conflicts with an existing close‑only order, the new order will fail. Switching the conflicting order to “reduce‑only” resolves the issue.

---

Order Price Limits

- The order price may deviate no more than 50 % from the current Mark Price.

- For reduce‑only orders, the price cannot breach the bankruptcy price of the position.

- For add‑to‑position orders, the price cannot exceed the liquidation price of the position.

If the price deviation is too large to get filled, consider lowering the leverage and resubmitting the order.

---

Illustrated Guide to Perpetual Contract Trading

---

This completes the comprehensive breakdown of gate.io’s perpetual contract rules. For additional tips on using gate.io and the latest platform updates, stay tuned to future articles from Bitaigen (比特根).

*Please note that cryptocurrency gains may be subject to tax in your jurisdiction. Consult a tax professional to understand your local obligations. If you are a U.S. resident, you must use Binance.US rather than the global Binance platform for any related fiat (USD, SEPA, SWIFT) transactions.*

Related Reading

- Funding-Rate Arbitrage Risks in Perpetual Contracts

- KiloEx: Near‑Zero Gas Ultra‑Smooth Order Execution & Dual‑Pool Risk Isolation fo

- Hyperliquid vs dYdX: Speed, DAO Governance & Market Edge

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.