In the painful throes of a bear market, selecting tokens that combine stable returns, a genuine ecosystem, and market recognition is especially critical. Using data from multiple platforms and a rigorous model to filter out noise, we lock in a handful of core assets that offer dividends and protocol revenue. This article presents a panoramic view of these potential projects, helping readers find value breakthroughs in a downturn. Please continue reading.

Which Tokens Should Be Monitored in a Bear Market? Core Conclusions First

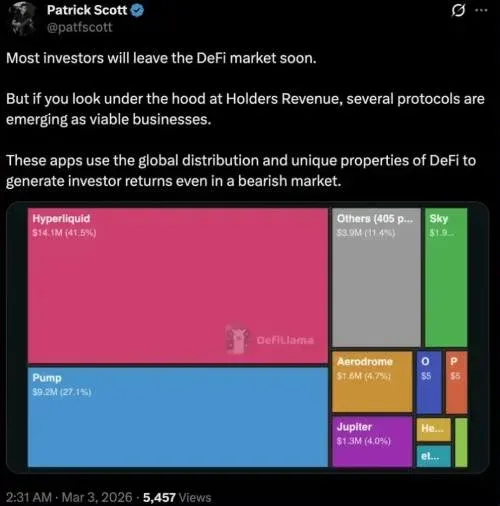

During the current crypto slump, the number of assets that truly meet the three standards of “delivering returns to holders, possessing protocol revenue, and having strong narrative and market recognition” is extremely limited. After screening 17,148 tokens, we arrived at 12 categories covering 132 investable projects, of which 45 are capable of distributing dividends to holders (low‑yield tokens have been excluded). Collectively, these generate an annualized cash flow of roughly USD 1.8 billion. Notably, the earnings of these 45 tokens are almost monopolized by Hyperliquid and Pump.fun, together accounting for ≈ 69 % of total holder returns.

---

Data Sources and Screening Methodology

This analysis primarily relies on DefiLlama, CoinMarketCap, as well as activity metrics from Dexu, Moni, Lunarcrush, and other platforms. To reduce personal bias, I employed Claude Code for most of the data processing. Although the debugging phase took roughly ten times longer than the writing itself, some margin of error may remain; the tables are for reference only, and full data links are provided at the end of the article.

During the filtering process I initially considered discarding legacy tokens such as XRP, ADA, BCH, but their multi‑cycle history and ample liquidity indicate they still possess survivability, so they remain on the final list.

---

1️⃣ Yield‑Sharing Tokens — The Most Worthy of Attention

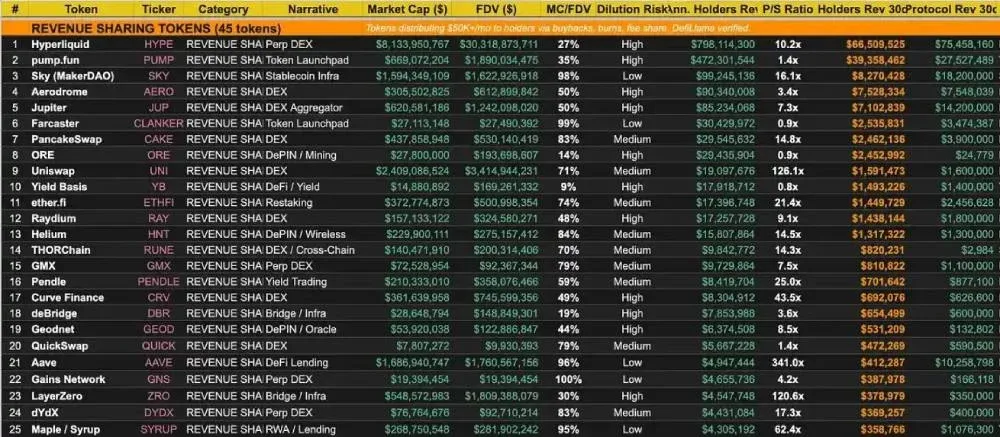

The prevailing market narrative today is “projects without revenue cannot survive,” and even ETH is increasingly judged by “value measured by income.” Consequently, tokens that return profit directly to holders via buy‑backs, burns, or fee sharing become the top candidates. We relaxed the screening threshold to DefiLlama’s 30‑day holder yield ≥ USD 50,000, resulting in 45 tokens that collectively deliver about USD 153 million per month to holders, or roughly USD 1.8 billion annually.

Top Ten Yield‑Sharing Tokens

Note: The “yield sharing” shown here does not equal the holder‑yield metric on DefiLlama. For example, EtherFi does not appear on the holder‑yield leaderboard yet returns value to holders through systematic buy‑backs.

It is worth mentioning that if crypto assets continue evolving toward a “token = stock” model, the price‑to‑sales (P/S) ratio will become a key valuation metric. The two projects below have P/S ratios below 4, making them appear extremely cheap from a traditional finance perspective. At current revenue rates, their market caps could be fully recouped in roughly 3 years:

- Pump.fun: 1.4×

- Aerodrome: 3.4×

In contrast, Uniswap (P/S ≈ 121) and Aave (P/S ≈ 341) command premium valuations due to market expectations about future upside, causing their price‑to‑sales figures to far exceed current earnings.

---

2️⃣ Projects with Protocol Revenue but No Dividends Yet

This category comprises 16 tokens whose monthly protocol revenue exceeds USD 100,000, with all earnings retained in the protocol treasury. Representative examples include:

- Lido: ~USD 4.3 million monthly revenue, TVL of USD 32 billion (has floated a staking‑dividend proposal)

- CoW Protocol: ~USD 3 million per month

- Meteora (Solana): ~USD 2 million per month

- Virtuals Protocol: ~USD 1.4 million per month

- Drift: ~USD 868,000 per month

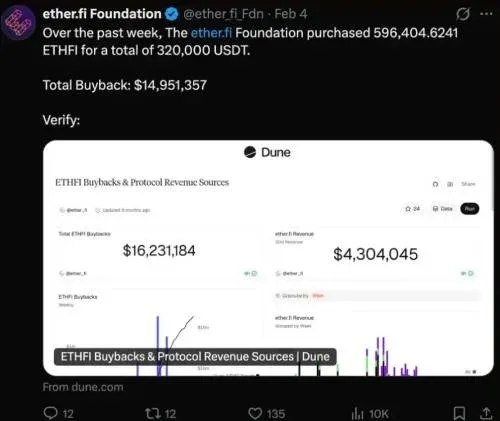

Comparing Lido with ether.fi: Lido’s TVL is ten times larger and its revenue three times higher, yet it does not distribute any earnings to LDO holders. Ether.fi, by contrast, returns roughly USD 1.5 million each month to holders via buy‑backs. In a bear market, preserving value clearly leans toward the latter.

The common logic among these protocols is the potential future activation of a “dividend switch.” Lido has repeatedly signaled this possibility, while Jito generates about USD 5.3 million in monthly fees, of which only USD 544,000 goes into the treasury. The gap between fee income and holder‑distributed revenue represents both opportunity and risk.

---

3️⃣ Quick Glance at Other Sectors

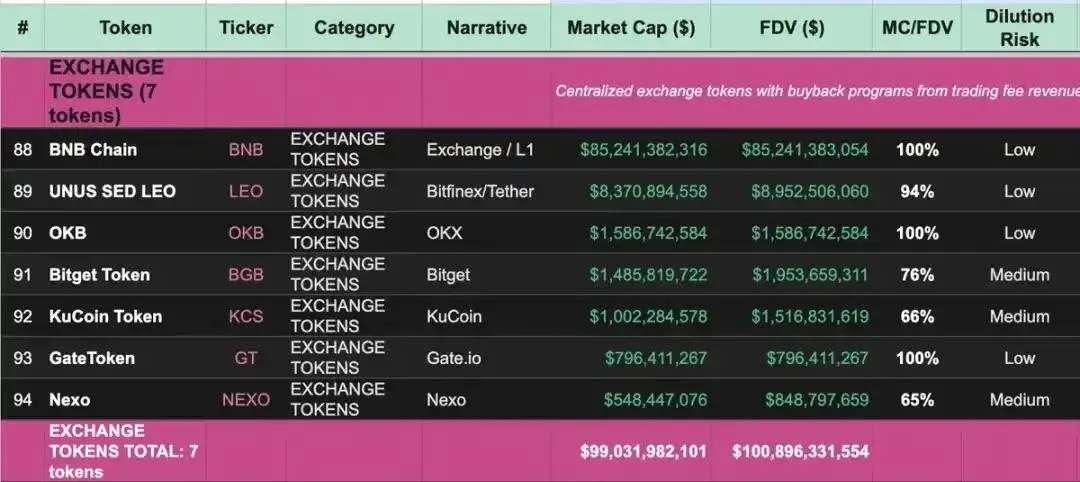

Exchange Tokens (7 tokens, total market cap ≈ USD 99 billion, includes BNB)

Whether in bull or bear markets, exchange tokens tend to have relatively stable revenue streams. Even if trading volume contracts, the revenue does not drop to zero. BNB alone commands a market cap of roughly USD 85 billion, while LEO and OKB experienced limited declines throughout the 2022‑2024 bear phase. Most of these tokens have buy‑back programs and a high circulating ratio, which further dampens downside risk.

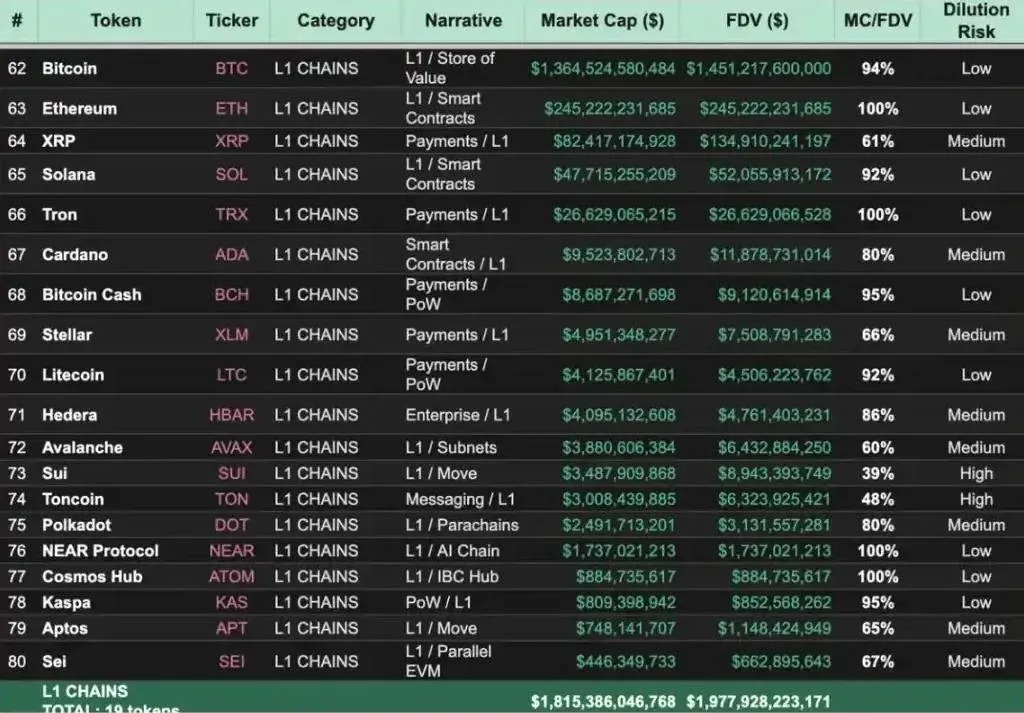

Layer‑1 Blockchains (19 tokens, total market cap ≈ USD 1.8 trillion)

- BTC: about USD 1.36 trillion

- ETH: about USD 245 billion

I relaxed the screening criteria for XRP, ADA, Cosmos because they have weathered multiple cycles, possess loyal communities, and enjoy ample liquidity. Even though some remain skeptical about TRX, it generates roughly USD 26 million in monthly fees—more than both Solana and Ethereum.

AI & Compute (8 tokens, total market cap ≈ USD 5.1 billion)

Most projects have yet to produce tangible revenue; the sole exception is Venice (VVV), which sustains buy‑backs and token burns through subscription and API fees, having already destroyed 43 % of its supply.

- Bittensor: market cap around USD 1.9 billion, hosts 128 subnetworks, currently no protocol revenue.

- Render, Akash: provide GPU compute leasing at costs lower than centralized providers.

- Grass: offers a decentralized data network for AI training.

Remark: Some AI tokens that did not make the list have posted sizable short‑term gains and may suit traders, but whether they qualify as “investable” remains a personal judgment.

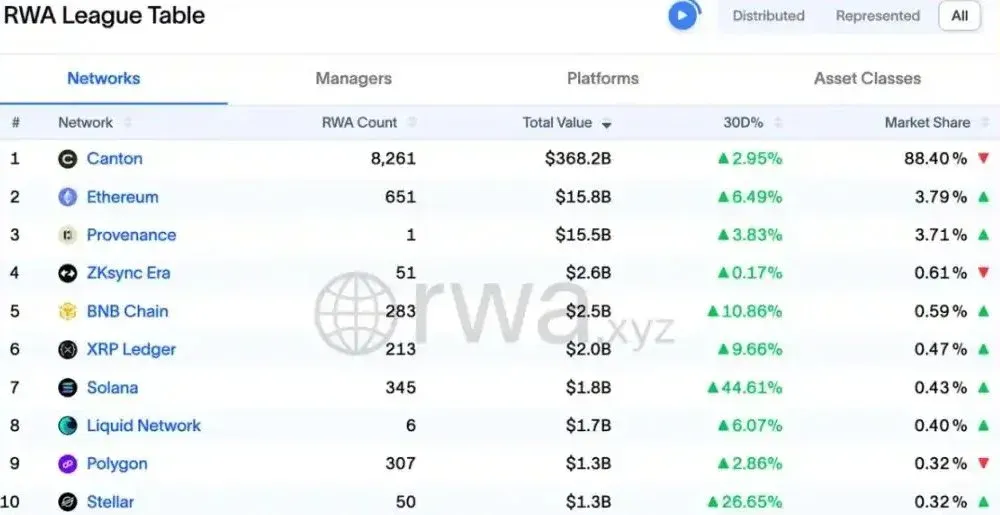

Real‑World Asset (RWA) Tokenization (7 tokens, total market cap ≈ USD 13.5 billion)

The sector is still growing quietly; a true bull market has not yet materialized. Canton Network has tokenized 88.57 % of its on‑chain RWA holdings, representing roughly USD 372 billion in assets, though the complexity of the underlying assets should not be underestimated.

Chainlink, as the core RWA oracle, distributes LINK staking rewards that stem from inflation and a fixed reward pool. The earnings primarily flow to node operators and the treasury, not directly to token holders.

Privacy Tokens (2 tokens, total market cap ≈ USD 9.7 billion)

Regulatory tightening raises risk in this space, yet demand remains relatively steady. Main projects:

- Monero (XMR): about USD 6.2 billion

- Zcash (ZEC): about USD 3.6 billion

Meme Coins (6 tokens, total market cap ≈ USD 20.8 billion)

Including them in an “investable” list is debatable, but their community‑driven nature can sometimes yield outsized performance during market rebounds compared with high‑yield tokens. Core members:

- DOGE: market cap about USD 15.2 billion, has existed for over a decade

- SHIB, PEPE, BONK, FLOKI, WIF also appear on the list.

Because there is no hard revenue ceiling, these tokens lack a clear valuation ceiling, and their high circulation rates limit sell‑pressure.

Other Sub‑Categories

- Layer‑2 Blockchains (7 tokens, total market cap ≈ USD 3.7 billion)

- DePIN (5 tokens, total market cap ≈ USD 500 million)

- Oracles / Infrastructure (7 tokens, total market cap ≈ USD 1.8 billion)

- Stablecoin Infrastructure (4 tokens, total market cap ≈ USD 1.1 billion), with Ethena leading the pack.

---

4️⃣ Extremely Profitable Projects That Have No Token

Several crypto‑related businesses generate revenue that dwarfs the total income of all listed tokens, yet they have no tradable token attached:

- Tether: annual revenue exceeds USD 6 billion, all going to shareholders.

- Polymarket: about USD 3.8 million monthly revenue, no token issuance.

- Base: profits flow to Coinbase shareholders; a token may be considered in the future.

- Phantom: user base in the tens of millions, generating substantial fee income.

- Circle (issuer of USDC): earnings will be reflected in its upcoming IPO.

- Kalshi: regulated by the CFTC, operates without a token.

- Farcaster: recently acquired; airdrop size may shrink, but a token could still materialize.

---

5️⃣ How to Use This Information for Positioning?

In a bear market, an ideal holding should satisfy four key criteria:

- Holders receive a tangible return.

- The price‑to‑sales (P/S) ratio is relatively low.

- The circulating‑market‑cap‑to‑fully‑diluted‑valuation (MC/FDV) ratio is high.

- Demand is sustainable.

Very few tokens meet all four simultaneously. The following list contains the relatively closest candidates:

| Token | P/S | MC/FDV |

|---|---|---|

| **PUMP** | 1.4 | 33 % |

| **AERO** | 3.4 | 50 % |

| **JUP** | 7.3 | 51 % |

| **SKY** | 16 | 98 % |

| **CAKE** | 15.1 | 96 % |

Lower‑Risk Options

- Exchange tokens: LEO, OKB, GT

These tokens are almost fully circulating and backed by exchange‑profit buy‑backs, offering relatively stable performance during a bear market.

Higher‑Risk, Higher‑Reward

- HYPE: revenue leads the pack, but MC/FDV is only 25 %, making it a highly volatile instrument. After Coingecko removed long‑term non‑circulating and burned tokens, the overall circulating proportion fell to 41 %.

Tradable Opportunities

Monitor governance developments and consider allocating to protocols that already generate revenue but have not yet switched on dividend distribution. Once the “dividend switch” flips, a revenue surge could follow. Projects to watch include Lido, Meteora, Drift, CoW Protocol.

---

Closing Thoughts

During a crypto bear market, the safest play remains holding Bitcoin (BTC), while allocating the remaining “play‑money” to explore new protocols and experiment with AI tools in anticipation of future opportunities. Whether you are bullish on AI compute on‑chain or believe RWA tokenization will keep growing, you must independently assess if the listed tokens constitute the best bets for you.

Note: Cryptocurrency gains may be taxable depending on your local jurisdiction. Be sure to consult a tax professional familiar with crypto‑related tax rules.

For U.S. readers: Trading on the global Binance platform is not available in the United States; you should use Binance.US or other U.S.-compliant exchanges. Fiat deposits and withdrawals typically use SEPA (for EUR) or SWIFT for other currencies, and all amounts are quoted in USD for consistency with the global

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.