When cryptocurrency is mentioned, many people immediately think of Bitcoin and Ethereum, while the stablecoin USDC often receives far less attention. So, what exactly is USDC, and how does it differ from other digital assets?

USDC is a type of stablecoin. As stablecoins gradually become a crucial bridge between the crypto world and traditional payment ecosystems, USDC—one of the most closely watched dollar‑pegged stablecoins on the market—has been drawing increasing interest from investors.

This article will systematically explain how USDC works, its common use cases, the differences with its main competitor (especially USDT), its strengths and weaknesses, and practical advice on buying, exchanging, and securely storing it.

From an industry‑wide perspective, we break down the technical foundation of USDC, its real‑world applications, and its core distinctions from USDT. We also consider regulatory compliance, on‑chain transparency, and provide actionable guidance to help readers make clearer judgments in the rapidly evolving stablecoin ecosystem.

Latest USDC News for 2025‑2026

March 5 2026

Tether announced a strategic partnership with a major U.S. payments network to embed its USAT token into retail point‑of‑sale terminals. The move accelerates USAT’s rollout in consumer‑payment scenarios and pushes forward the integration of USDC‑type stablecoins across similar payment infrastructures.

February 10 2026

Circle revealed the launch of a cross‑border payment pilot that teams up with several European and Asian financial institutions. The program aims to achieve instantaneous settlement and real‑time fund arrival, boosting the efficiency of stablecoins in international trade and corporate payments.

January 20 2026

The U.S. Federal Reserve updated its stablecoin regulatory guidance, providing clearer rules on reserve transparency and liquidity requirements. The new guidance obliges major dollar‑backed stablecoins such as USDC and USAT to periodically disclose asset composition and liquidity test results, in order to strengthen investor confidence and promote orderly markets.

December 8 2025

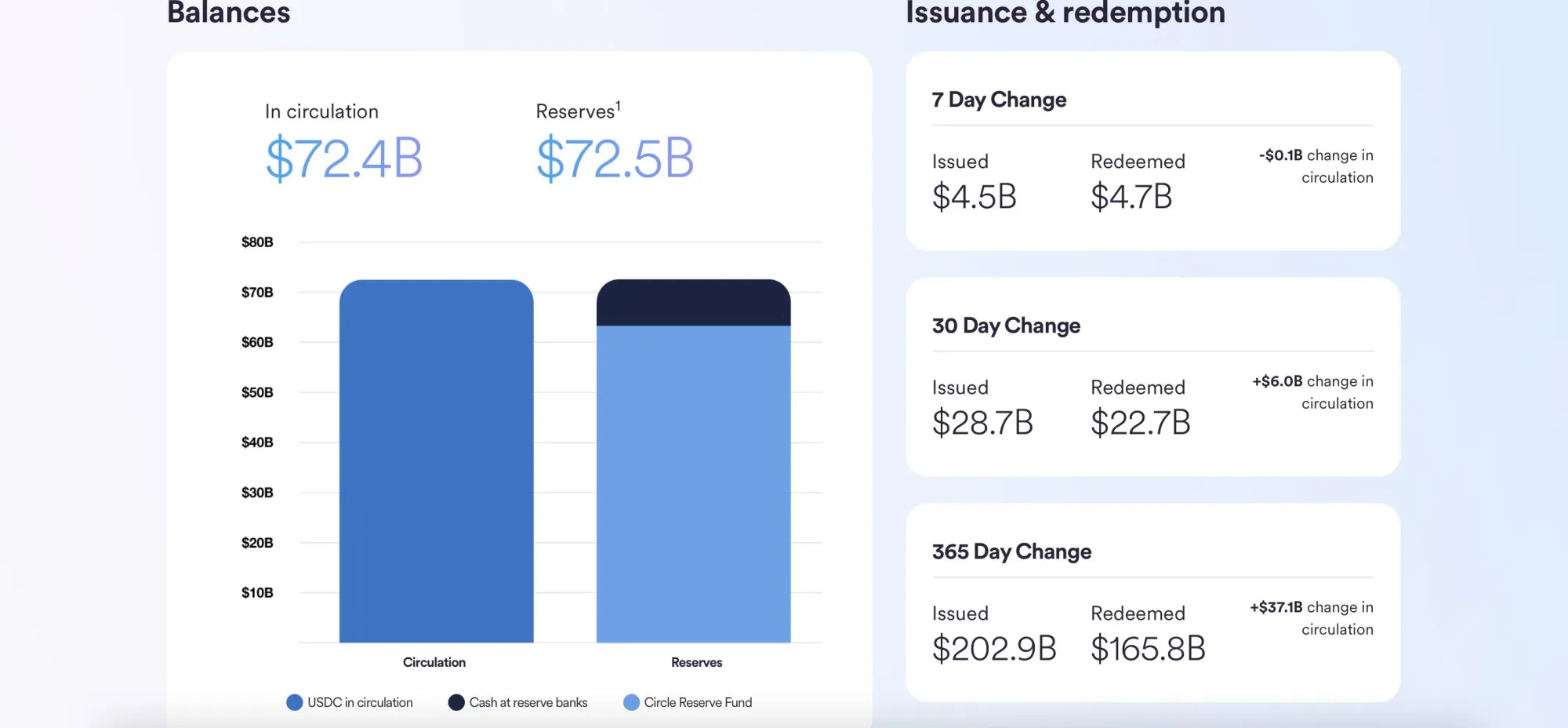

Circle published its Q4 2025 financial results, reporting that USDC’s circulating supply surpassed 650 billion tokens. Despite facing new competitors and regulatory pressure, USDC continued to grow steadily, reflecting persistent demand across trading, payments, and DeFi sectors.

November 15 2025

Tether completed the first public offering of its U.S.‑based stablecoin USAT, receiving approval from U.S. regulators. USAT’s launch on multiple exchanges and payment platforms enhances Tether’s legitimate competition in the domestic market, potentially pressuring USDC’s market share.

October 22 2025

Circle partnered with leading DeFi protocol Forge Finance to integrate USDC into a cross‑chain lending and staking platform, increasing USDC’s utility across multiple blockchain ecosystems and reinforcing its role in DeFi borrowing and yield strategies.

September 16 2025

Circle expanded its collaboration with Hyperliquid, deploying USDC natively on a new trading and liquidity protocol. This step further promotes USDC adoption within DeFi and trading infrastructure, widening its use cases and network effect.

September 12 2025

Tether announced the launch of the U.S.‑centric stablecoin USAT, taking a compliance‑first approach and positioning itself as a direct competitor to USDC. Operating under the latest regulatory framework, USAT intensifies competition and regulatory linkage in the stablecoin market, with strategic implications for USDC’s positioning.

August 13 2025

Circle disclosed a 10 million‑share secondary placement plan, which caused a short‑term dip in its stock price. The plan involved both company‑initiated sales and existing shareholder disposals; market volatility reflected concerns about dilution and the financial health of the USDC issuing entity.

July 18 2025

U.S. President signed the GENIUS Act, establishing a federal‑level regulatory framework for stablecoins. The legislation codifies reserve requirements, periodic disclosure obligations, and other compliance measures, directly affecting dollar‑backed stablecoins—including USDC—by shaping their legal environment.

June 5 2025

Circle completed its initial public offering (IPO) on the New York Stock Exchange under the ticker CRCL. The listing dramatically increased the public visibility and capital strength of USDC’s issuer, signaling the stablecoin’s entrance into mainstream finance.

What Is USDC?

USDC (USD Coin) is a stablecoin issued and managed by Circle, pegged 1:1 to the U.S. dollar. In plain language, USDC is a digital dollar on the blockchain.

Think of USDC as an electronic version of a physical U.S. banknote—for every 1 USDC minted, an equivalent of 1 USD (or an asset of equal value) is held in a bank or a regulated financial institution. This “1 : 1 dollar reserve” mechanism generally keeps USDC’s market price close to $1.00.

In June 2025, Circle became the first publicly listed stablecoin issuer on the NYSE (ticker CRCL). Its debut share price surged 168 %, pushing the company’s market capitalization above $30 billion, marking USDC’s formal arrival on mainstream financial radar.

On Which Blockchains Is USDC Issued?

USDC debuted on Ethereum as an ERC‑20 token. As demand grew, Circle expanded USDC to multiple public blockchains, allowing users to select the network that best fits their needs.

As of 2025, USDC is available on the following major blockchains:

- Ethereum – the original chain, offering the deepest liquidity.

- Solana – high‑throughput, low‑fee environment suited for micro‑payments.

- Polygon – an Ethereum scaling solution that combines low cost with compatibility.

- Avalanche, Arbitrum, Optimism, and other emerging networks – provide faster transaction experiences and further broaden USDC’s reach.

Basic Facts About USDC

How Does USDC Operate?

USDC’s core workflow consists of three stages—minting, reserving, and redemption—which together maintain its 1:1 dollar peg. Below is a step‑by‑step breakdown:

Minting USDC

Investors or institutions transfer fiat dollars into Circle’s designated bank accounts. Circle then creates an equivalent amount of USDC on the blockchain. For example, depositing $100 yields 100 USDC.

Reserving USDC

The deposited dollars are placed in regulated bank accounts or invested in high‑quality, low‑risk assets such as U.S. Treasury securities. Circle publishes regular audit reports, publicly demonstrating that every issued USDC is fully backed by dollars or dollar‑equivalent assets.

Redeeming USDC

When a holder wishes to convert USDC back into fiat, they return the tokens to Circle. The system burns the corresponding USDC and transfers the equivalent USD back to the user’s bank account.

Tax note: In many jurisdictions, including the United States, gains or losses realized from converting USDC to fiat or other crypto assets may be subject to capital‑gains tax. Users should consult local tax regulations or a qualified tax professional.

Use Cases for USDC

Crypto Trading and Investment

Within crypto exchanges and investment platforms, USDC is commonly treated as a stable “safe‑haven” asset. During periods of high volatility, traders often swap volatile tokens for USDC to lock in value and avoid short‑term price swings.

Numerous regulated exchanges—such as Coinbase and Kraken—support USDC extensively; USDC trading pairs account for roughly 40 % of activity on these platforms, making it especially friendly for newcomers and ensuring ample liquidity.

USDC is also frequently used in dollar‑cost averaging (DCA) strategies: investors purchase a fixed amount of USDC at regular intervals and later convert it into target cryptocurrencies when market conditions appear favorable, thereby smoothing entry‑price risk.

Decentralized Finance (DeFi)

In the DeFi ecosystem, USDC stands out as one of the most widely utilized stablecoins for lending, liquidity provision, and yield farming.

- Lending & Borrowing – Depositing USDC into protocols like Aave or Compound yields relatively stable interest rates, typically ranging from 3 % – 5 % APR.

- Liquidity Mining – Supplying USDC to automated market maker (AMM) pools earns a share of trading fees and platform incentives. New users are advised to stick with audited, high‑liquidity platforms to mitigate smart‑contract and counter‑party risks.

- Cross‑Chain Expansion – In June 2025, USDC launched on the XRP Ledger, enabling trading and synthetic asset creation on that chain’s DEX. While this broadens USDC’s DeFi footprint, it also introduces bridge‑related and network‑specific security considerations.

Cross‑Border Remittances and Payments

Sending money internationally with USDC follows a straightforward workflow:

- Sender converts local fiat into USDC.

- Blockchain transfer moves USDC to the recipient’s wallet.

- Recipient redeems USDC for local fiat.

By bypassing multiple traditional banking intermediaries, this method usually incurs lower fees and reduces settlement time from the conventional 3 – 5 days to a matter of minutes.

Emerging markets such as Brazil and Mexico have seen digital‑bank platforms begin to support stablecoin corridors, giving local users easier access to dollar‑denominated value and easing cross‑border friction.

Practical considerations still depend on the availability of on‑ramps/off‑ramps, exchange spreads, platform fees, and the regulatory/KYC requirements of the jurisdictions involved. These factors are essential when planning real‑world transactions.

Everyday Payments

USDC’s utility for everyday purchases is gradually expanding. In June 2025, Shopify announced native support for USDC payments, allowing millions of merchants worldwide to add a “crypto payment” option at checkout. Customers can pay directly with USDC, avoiding the need to first convert back to fiat, which shortens settlement time and cuts cross‑border conversion costs.

Beyond e‑commerce, an increasing number of payment‑card and wallet providers are developing features that instantly convert stablecoins to fiat at the point of sale. This enables users to hold USDC in a mobile wallet and automatically swap it for local currency when paying in‑store or online.

Adoption, however, remains limited by merchant acceptance, regional regulatory stances, and tax reporting obligations. For merchants, deciding whether to accept USDC directly or convert it immediately into fiat will affect both exchange‑rate risk and accounting treatment.

USDC vs. USDT

When stablecoins are discussed, USDT (Tether) is often the first name that comes to mind, given its dominant market position. While both USDC and USDT are dollar‑pegged, they differ in issuance mechanics, transparency, compliance focus, and market dynamics.

- Issuance & Reserve Disclosure – Circle (USDC) commissions major accounting firms each month to produce reserve attestations following AICPA standards, publishing the composition on its website to bolster institutional and regulator confidence.

- Transparency – Historically, Tether faced scrutiny over the exact nature of its reserves. Although recent disclosures have improved, USDC still enjoys a clearer audit trail.

- Market Size – As of September 17 2025, USDT’s market cap remained substantially larger than USDC’s (approximately $170 billion vs. $73 billion), giving USDT deeper order books and broader pair coverage.

- Compliance & Institutional Adoption – USDC’s emphasis on auditability and regulatory compliance makes it a preferred choice for many institutions. Both tokens pursue multi‑chain deployments, but USDC stresses native multi‑chain issuance and transparent reserve management, whereas Tether leverages its scale and liquidity to maintain market dominance.

USDC Compared With Other Stablecoins

From a broader perspective, stablecoins fall into several categories. USDC belongs to the fiat‑collateralized group, meaning a fiat currency (or equivalent assets) backs each token, managed centrally by the issuing entity, which promises a 1:1 redemption.

Other common categories include:

Compared with crypto‑collateralized or algorithmic stablecoins, USDC’s advantages are higher transparency, strong compliance orientation, and broad institutional uptake. Its drawbacks stem from reliance on a single issuer and the centralized nature of its reserve holdings.

Four‑Stablecoin Comparison

Pros and Cons of USDC

Advantages

- High Transparency – Regularly published reserve data and third‑party audit reports.

- Strong Compliance Focus – Favoured by regulated platforms and institutional participants.

- Price Stability – Theoretically maintains a 1 USDC = 1 USD ratio, suitable for value preservation.

- Multi‑Chain Availability – Native support across several blockchains simplifies transfers and smart‑contract interactions.

- Broad Adoption – Used in trading, DeFi, cross‑border payments, and merchant settlement.

- Easy Conversion – Major exchanges and wallets provide robust on‑ramps and off‑ramps.

Disadvantages

- Centralization Risk – Managed by a single issuer; reliance on its operational health and partner banks.

- Reserve Asset Risk – Reserves are often held in short‑term instruments; interest‑rate or market fluctuations could affect the issuer’s risk profile.

- Regulatory Uncertainty

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.