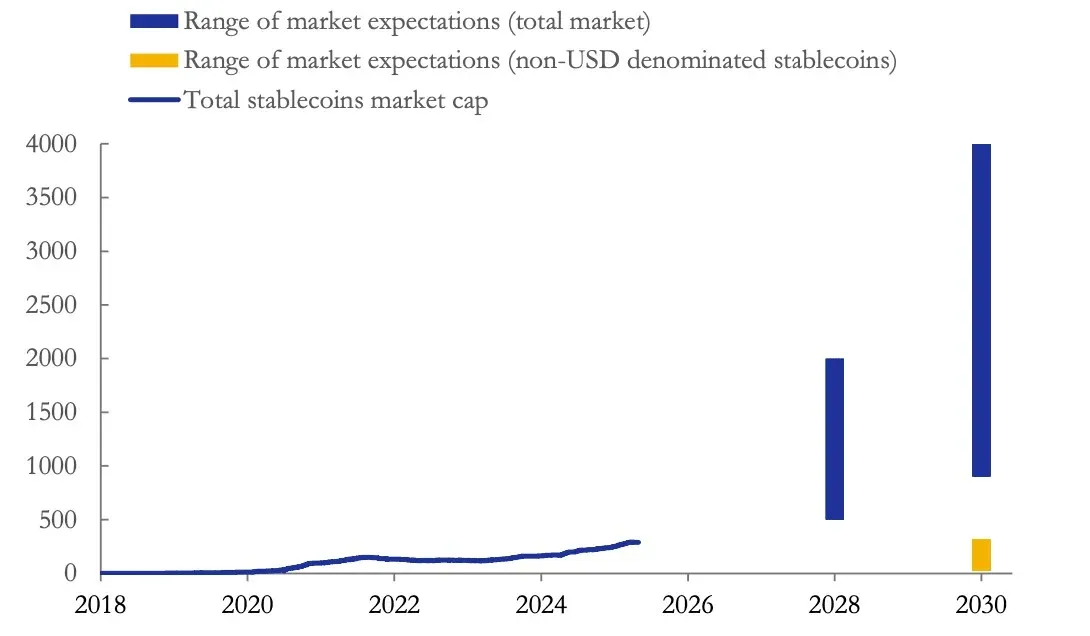

Over the past three years, the total market capitalisation of stablecoins has doubled from roughly USD 1.56 billion to USD 3.12 billion. The European Central Bank’s (ECB) working paper projects that the figure could climb to about USD 2 trillion by 2028. This rapid expansion has drawn close regulatory scrutiny concerning its potential macro‑economic impact.

This article provides an in‑depth analysis of the ECB’s warning about the macro‑financial risks posed by stablecoins, explains how they could undermine the transmission of euro‑area monetary policy and bank lending, helps readers understand the regulatory trajectory and possible shocks to the financial system, and explores the prospective effects on cross‑border payment dynamics. Continue reading for the details.

The Euro‑Area Money Structure Is Crucial

The report notes that if foreign‑currency‑denominated stablecoins continue to infiltrate the market—especially in environments dominated by non‑euro tokens—the transmission chain between domestic monetary policy and bank loans could be weakened, amplifying systemic risk. ECB officials have previously warned that the expansion of USD‑denominated stablecoins may erode the euro’s dominance in cross‑border payments and even spark debates over monetary sovereignty.

Data cited in the working paper show that USD‑backed stablecoins virtually monopolise the sector. According to CoinGecko, tokens pegged to the US dollar hold a market capitalisation of USD 301 billion, accounting for 97 % of total stablecoin value. This concentration implies that the euro‑area financial system could face a larger external shock when confronted with dollar‑denominated digital assets.

Stablecoin Impact: Banks, Monetary Policy, and Currency Importance

To assess how this trend could affect the traditional banking system, the ECB highlights the “deposit substitution effect.” When households and firms shift funds from retail‑bank deposits into digital assets, banks lose a low‑cost, relatively stable source of funding. The report states: *“Banks rely heavily on deposits to support lending to households and businesses.”* If deposit volumes contract, banks may be forced to depend more on wholesale or market‑based financing channels, which typically carry higher costs and less stability.

At the same time, the report points out that widespread stablecoin usage could alter the transmission of policy rates to bank funding costs and loan pricing. The authors explain: *“Our research finds that the adoption of stablecoins interferes with multiple monetary‑policy transmission channels, reducing the predictability of policy actions.”* This impact is not linear; its magnitude depends on the scale of stablecoin adoption, technical design, and the regulatory framework in place.

Actual and expected developments in the stablecoin market. Source: European Central Bank (Citigroup, Coinbase, JPMorgan)

Conclusion

In summary, the ECB cautions that as stablecoins become more prevalent, capital may flow out of traditional bank deposits, weakening the transmission of monetary policy to loans and posing a potential challenge to financial stability in the euro area. For further analysis and updates on this topic, stay tuned to Bitaigen’s (比特根) ongoing coverage.

Note for U.S. readers: When accessing cryptocurrency services, use Binance.US rather than the global Binance platform. For fiat on‑ramps outside the United States, SEPA (for euros) and SWIFT (for other currencies) remain the primary settlement networks.

*Crypto gains may be taxable in your jurisdiction; consult a local tax professional for guidance.*

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.

⚠️ Risk Disclaimer: Crypto prices are highly volatile. This is not investment advice.