In this article we systematically outline the core principles and operating mechanisms of prediction markets, revealing how ordinary investors can, in an environment dominated by bots and market makers, combine subjective judgment with technical tools to construct viable arbitrage ideas. Through practical record‑keeping, semi‑automated monitoring, and low‑stake testing guides, readers are helped to get started quickly and continuously refine their strategies while keeping risk under control.

4. Summary and Actionable Guidance

Prediction markets are saturated with highly efficient automated bots and professional market makers that capture the bulk of profits by leveraging algorithmic advantages. For a regular participant to maintain a foothold in such a competitive environment, it is necessary to blend subjective judgment with technical assistance to forge a marginal edge.

- Record‑keeping and Review: After every order, log the full position size, hedging details, and settlement outcome. Then check whether the sum of the Yes/No contract prices deviates significantly from 1, or whether a price inversion anomaly appears.

- Semi‑automated Monitoring: Use existing market‑data tools or write custom scripts to capture odds discrepancies in real time and trigger alerts, thereby improving reaction speed.

- Low‑Stake Testing: Execute the complete prediction‑market bet + perpetual‑contract hedge workflow with a very small amount of capital to verify strategy feasibility and accumulate practical experience.

Remember, arbitrage is not risk‑free; it must be paired with strict risk management and a commitment to ongoing learning.

1. Core Concept Review

The essence of a prediction market is the trading of probabilities for events that are about to occur, rather than gambling in the traditional sense. Participants buy and sell “contracts” to express their view on an event’s outcome; the contract’s value ultimately depends on whether the event materializes.

For example, if the market is focusing on “Will Joe Biden win the 2024 U.S. presidential election,” the platform will issue two binary contracts: Yes and No. If the Yes contract is quoted at $0.60, the market collectively assigns roughly a 60 % probability to Biden’s victory.

This binary (yes/no) design enables information to aggregate quickly into prices, improving the overall accuracy of the forecast. Multi‑outcome events can be handled by extending the contract types accordingly.

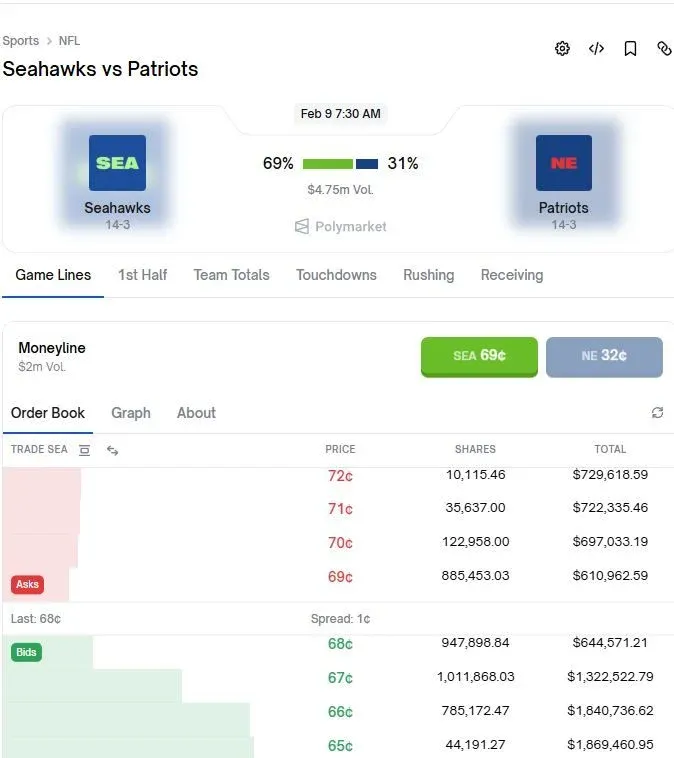

2. How the Order‑Book Model Works

Platforms such as Polymarket employ a Central Limit Order Book (CLOB), a mechanism similar to traditional equity exchanges. Buyers and sellers submit limit orders, and the system matches them continuously, forming the best bid (Buy) and best ask (Sell) prices.

Within this framework, contract prices are no longer set by a fixed algorithm; they are shaped instantly by market supply and demand. Although, in theory, the price should reflect the event’s true probability, actual trading is often disturbed by FOMO, independent information sources, or market‑maker actions, creating short‑term deviations. These mispricings are precisely the entry points that arbitrageurs can exploit.

3. Common Arbitrage Techniques

Prediction markets present a variety of potential price‑difference opportunities, and participants generally fall into two roles:

- Market Makers / Liquidity Providers: Purchase the undervalued side and sell the overvalued side when odds become extreme, then close the position when prices revert to a more rational level.

- Direction‑Neutral Arbitrageurs: Simultaneously place a bet in the prediction market and hedge directional exposure with a perpetual futures contract; the focus is on capturing odds discrepancies rather than betting on price direction.

Below are several concrete, operational strategies. All of them involve costs such as fees, slippage, and liquidity constraints, which must be factored into any profitability calculation.

3.1 Identifying Value Mismatches

On platforms like Polymarket, contract prices are determined in real time by user supply and demand, with no house‑set fixed odds. Sentiment swings often warp prices. By scanning a large number of events and combining the scan with one’s own assessment of the underlying event, a trader can spot situations where the market price diverges from the “true” probability and take the undervalued side.

Risk note: If market sentiment continues to drift away from reality or your probability estimate is wrong, losses may occur.

3.2 In‑Platform Probability Hedging

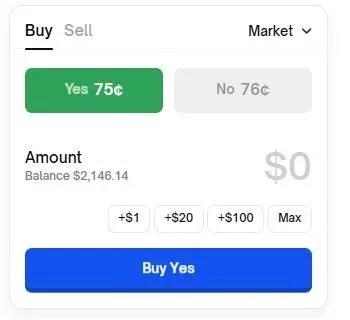

The basic principle is that for a single event the combined price of the Yes and No contracts should theoretically equal 1 (the same holds for multi‑outcome events when summed across all outcomes). When a deviation appears, an arbitrage opportunity arises.

- Total > 1 (the market over‑prices the event): short the contract with the higher valuation and lock in the spread.

- Total < 1 (the market under‑prices the event): buy all possible outcomes; at settlement you will receive at least $1, guaranteeing a profit after fees.

When executing these trades, consider the following costs:

- Transaction fees (often charged in USD)

- Slippage from large orders

- Platform limits on order size or position exposure

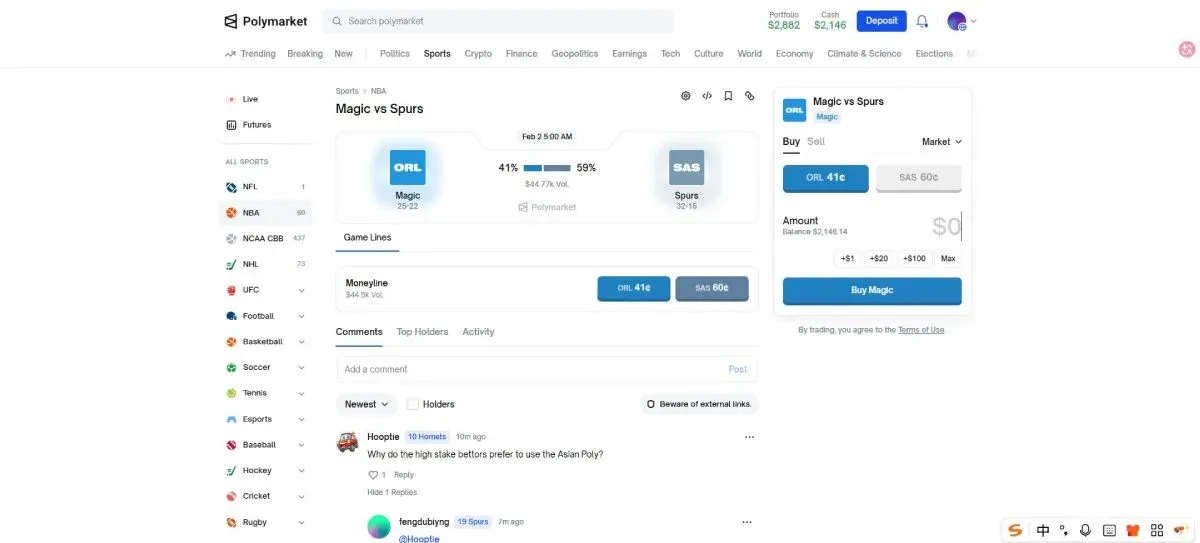

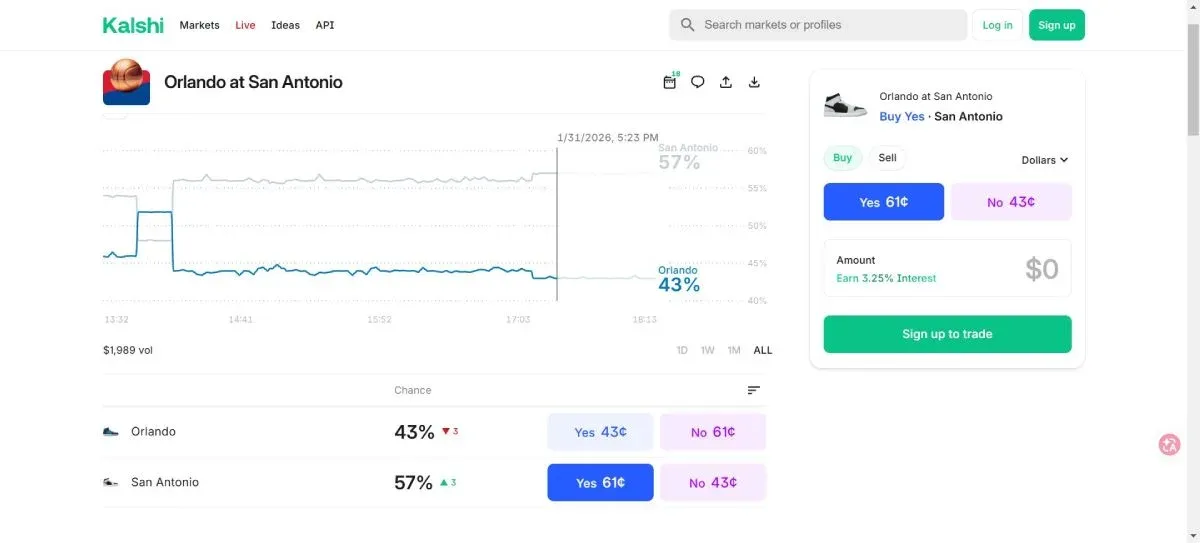

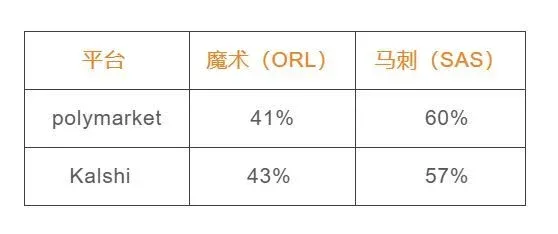

3.3 Cross‑Platform Odds Hedging

The same event listed on different platforms (e.g., Polymarket versus Kalshi) frequently shows disparate odds. If Platform A offers a higher quote for “Event Happens” while Platform B offers a higher quote for “Event Does Not Happen,” and the event definitions are identical, you can place synchronized orders on both sides to capture the spread.

The following example illustrates a real‑world odds comparison between two platforms:

Assume you buy the “Magic Team Wins” contract on Platform B for $0.41 and the “Spurs Win” contract on Platform A for $0.57, for a combined cost of $0.98. Whichever team ultimately wins, the settlement will pay $1.00, yielding a net profit of $0.02, or roughly 2 % return.

In practice, you must account for transaction fees, cross‑platform transfer costs (e.g., SEPA or SWIFT for fiat movements), and any settlement‑time differences. Ensure that the event description is exactly the same on both platforms before executing the trade.

Important for U.S. users: When moving fiat or crypto between exchanges for cross‑platform arbitrage, use Binance.US (or another U.S.-compliant exchange) instead of the global Binance platform to remain within regulatory boundaries.

5. Closing Remarks

Prediction markets aggregate collective intelligence to provide probability‑based pricing for uncertain events. Understanding their operating mechanics, order‑book characteristics, and typical price‑gap opportunities is a prerequisite for any arbitrage attempt. By coupling AI‑assisted tools with deep personal knowledge of specific domains, traders can carve out a niche even amid bots and professional market makers.

For those wishing to deepen their practical skills in prediction‑market trading, search for historical articles from Bitaigen or continue browsing the related content linked below. We look forward to your continued interest and support.

*Disclaimer*: Cryptocurrency and prediction‑market gains may be subject to taxation in your local jurisdiction. Always consult a qualified tax professional and adhere to applicable laws.

Related Reading

- LLMs & Crypto Drive Explosive Growth in Prediction Markets

- Polymarket Wallet Study Reveals 87% Users Lose Money

- Cryptocurrency Trading Price Gaps: Why Coins Vary Across Exchanges

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.