In this article we systematically outline the core principles and operational workflow of cash‑and‑carry arbitrage, helping readers understand why price differentials naturally converge and generate profit. Through case analysis and risk‑highlighting points, you can quickly assess when it is appropriate to deploy this direction‑neutral strategy. Subsequent sections will delve into key practical implementation techniques, making a thorough read worthwhile.

Educational: What Is Cash‑and‑Carry Arbitrage? Why Can This Trade Produce Profit?

Cash‑and‑carry arbitrage (also known as cash‑and‑carry hedge) refers to buying an asset in the spot market while simultaneously short‑selling an equivalent amount of futures contracts. Profit is earned from the convergence of the futures premium, because the price gap must collapse to zero at contract expiry, delivering a return without directional market risk.

What Is Cash‑and‑Carry Arbitrage

If you have ever traded futures contracts, you will have noticed that their trading price often diverges from the spot price of the underlying. When the futures price is higher than the spot price, the market is said to be in contango (a premium). In this situation traders can execute a cash‑and‑carry arbitrage (also called basis trading) to capture the premium. Conversely, when futures trade below spot, the market is in backwardation, prompting different arbitrage approaches.

The steps for a cash‑and‑carry arbitrage are:

- Buy the underlying asset in the spot market (e.g., Bitcoin).

- Short an equal quantity of futures contracts.

The short futures position hedges the long spot position, so fluctuations in the underlying’s price have little impact on the overall P&L. The trader then simply waits for the spread between spot and futures to narrow.

Why This Trade Can Be Profitable

Futures contracts have a fixed expiration date, and settlement is based on the spot price (or an average thereof). Consequently, as the expiry approaches, the premium embedded in the futures contract gradually disappears, ultimately reaching zero. Traders do not need to forecast the future price of the asset; they only need to exploit the inevitable convergence of the spread.

- Premium decay to zero: As the expiration date draws near, the difference between spot and futures prices must converge to zero.

- Early exit: In practice the premium often shrinks to near‑zero well before expiry, allowing traders to close the position early and lock in profit.

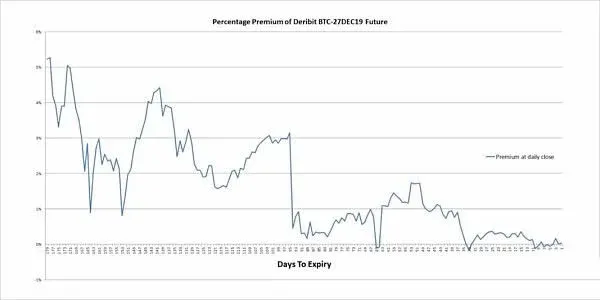

The figure below shows the percentage premium of Deribit’s Bitcoin futures contract (BTC‑27DEC19) relative to the spot market over roughly six months in December 2019.

The chart illustrates that the premium fluctuated sharply during the contract’s life, but as the delivery date approached the premium clearly trended toward zero. This is typical for Bitcoin futures and is similarly observed in many other contracts.

The essence of cash‑and‑carry arbitrage is: open the position when the futures contract shows a sizable contango, then unwind the trade once the premium collapses to zero. In this way the trader captures the premium without bearing price risk on the underlying asset.

A Concrete Example

At the time of writing, the BTC spot price on Coinbase was about $8,800, while the June futures contract on Deribit was trading around $9,190, creating a premium of roughly $390 (about 4.4 %).

The execution steps are:

- Purchase 1 BTC on the spot market for $8,800.

- Short 1 BTC June futures contract on Deribit at $9,190.

After establishing the positions, the trader simply waits for the spread between spot and futures to narrow. Regardless of whether Bitcoin’s overall price rises or falls, profit is realized as long as the premium contracts.

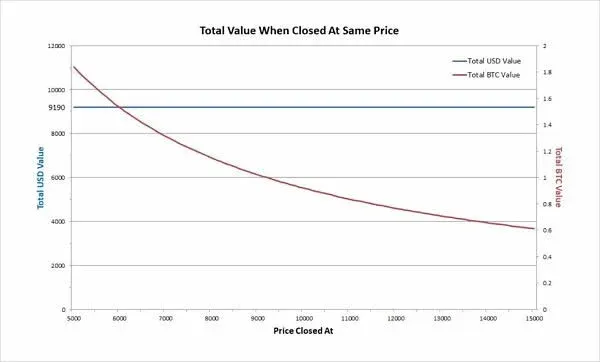

Assume that after a few weeks the premium has vanished, meaning the futures price now equals the spot price. The trader can then close the position. The chart below depicts the total value of the account in USD and BTC at the moment of closing (the exact USD amount depends on the BTC price at that time).

- Position snapshot: Initially $8,800 is used to acquire 1 BTC, which then serves as collateral for the short futures.

- Value preservation: No matter how Bitcoin’s price moves, the total portfolio value expressed in USD remains $9,190.

Illustrative outcomes:

- If BTC is $5,000 at closing, the short futures yields a profit of 0.838 BTC. The account now holds 1 + 0.838 = 1.838 BTC, valued at 1.838 × 5,000 = $9,190.

- If BTC climbs to $10,000, the short futures incurs a loss of 0.081 BTC. The remaining balance is 1 − 0.081 = 0.919 BTC, valued at 0.919 × 10,000 = $9,190.

The P&L formula for the futures short is:

```

(open price / close price – 1) × BTC position size

```

The order of operations when exiting:

- First, close the short futures position by buying back the same contract size.

- Then, sell the remaining BTC on the spot exchange for USD.

Because the trade is closed when the premium has reached zero, the BTC market value exactly matches the futures settlement price of $9,190, delivering a net gain of $390 without any directional exposure.

Tax note: In many jurisdictions, profits from cryptocurrency arbitrage are taxable events. Traders should consult local tax regulations and consider reporting obligations for any realized gains.

Some Practical Details About Cash‑and‑Carry Arbitrage

- Risk overview: The long spot and short futures legs are fully hedged, so price volatility has minimal effect on overall profit. Nonetheless, margin must be posted on the exchange, introducing margin‑related risk.

- Leverage usage: Low leverage reduces the amount of capital tied up as margin—for example, posting only 33 % of the required funds can maintain the position. High leverage further reduces margin usage but dramatically raises liquidation risk.

- Margin ratio: The higher the proportion of your capital allocated as margin, the closer the liquidation price is to the current market price. In an extreme case where all available funds are used as margin, the chance of a forced liquidation becomes negligible.

When to Close the Position

The most common practice is to wait for the premium to decay to zero before exiting, which often occurs naturally before contract expiry. Two additional early‑exit scenarios exist:

- Premium already zero: The futures price has aligned with the spot price; the trader can instantly buy back the futures contract and convert the BTC to cash.

- Premium turns negative (backwardation): Futures trade below spot, meaning the cash‑and‑carry position is at its most valuable; closing at this point maximizes profit.

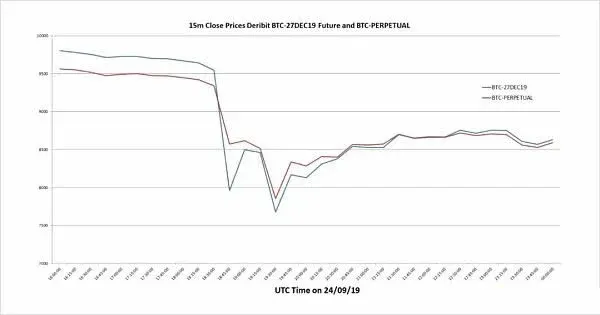

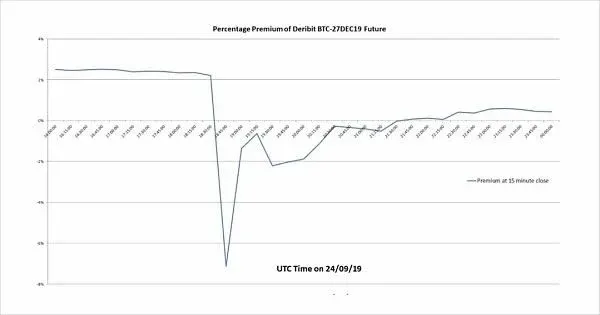

Case in point: on 24 September 2019, Deribit’s BTC‑27DEC19 contract and its perpetual contract experienced a rapid shift into backwardation. Early in the day the market was still in contango, but a sharp price drop later turned the premium negative, offering an excellent closing opportunity for traders holding the arbitrage position.

Rolling the Position (Contract Rollover)

After closing a contract, if the next‑month futures still exhibit a premium, a trader can immediately open a short on the new contract without first withdrawing the BTC to a spot exchange. This “roll” offers several advantages:

- Lower fees: Derivatives exchanges typically charge lower transaction fees than spot venues.

- No on‑chain transfers: Saves time and avoids the friction of withdrawing and redepositing coins.

- Capital efficiency: As long as the new contract’s spread is attractive, the same capital can continue to be employed for arbitrage.

Whether to roll depends on the size of the premium in the new contract and the desired duration of capital deployment.

Additional Considerations

- Capital opportunity cost: Cash‑and‑carry arbitrage ties up a relatively large amount of capital for a modest return, often lower than directional trading strategies. For instance, a 4 % premium that takes nine months to realize translates to an annualized return of roughly 5.3 %, which may be less attractive than other investment avenues.

- Asset safety: It is advisable to keep the bulk of your crypto holdings in a personal hardware wallet (e.g., Trezor or Ledger) and only transfer the amount needed for margin to the exchange, reducing exposure to exchange‑related risks.

- Exchange characteristics: Deribit enforces a price‑band limit of ±8 % to curb extreme price swings that could trigger mass liquidations. Even so, high leverage is discouraged; maintaining a prudent safety buffer remains essential.

Summary

Cash‑and‑carry arbitrage is a low‑risk arbitrage technique that offers limited but relatively stable returns. By leveraging automation tools, investors can perform a single entry and exit each month and capture a respectable yield while freeing up time for other, potentially higher‑value research. If you prioritize steady, risk‑adjusted income, cash‑and‑carry arbitrage should be considered among the primary strategies in your toolbox.

The above constitutes the full analysis of “Educational: What Is Cash‑and‑Carry Arbitrage? Why Can This Trade Produce Profit?” For more content on cash‑and‑carry strategies, please follow additional articles by Bitaigen.

---

Appendix Links

- Original article:

https://insights.deribit.com/education/cash-and-carry-trades/

Related Reading

- Liquidity Mining in DeFi: Risks & How to Safeguard Funds

- Dual‑Currency Win: High‑Sell & Low‑Buy Strategies Explained

- Ethereum Spot ETF: Listing Date, Brokers & Guide

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.