The Bitaigen editorial team believes that the design of stablecoins is not an esoteric mystery. By starting from a banking model, we present the collateral structures, peg mechanisms, and risk points of USDT, DAI, FEI, Basis Cash, and ESD in a clear, visual way. Chart‑driven analysis helps readers quickly differentiate centralized from decentralized approaches; once the core principles are understood, they can dive into the finer details.

Stablecoins: A Visual, Comprehensive Analysis of USDT, DAI, FEI, Basis Cash, and ESD

This article visually presents the underlying logic, collateral methods, and peg mechanisms of five stablecoins— USDT, DAI, FEI, Basis Cash, and ESD—so readers can quickly grasp how each operates.

Is a fully decentralized stablecoin a contradiction in terms? It is still too early to draw a definitive conclusion.

Over the past year, the circulating supply of stablecoins has exploded, yet only a small fraction of market participants truly understand how they work.

Many projects embed complex equations and industry‑specific jargon in their whitepapers, as if to suggest that “you are not smart enough” to follow. In reality, the underlying design of all stablecoins is remarkably straightforward. The visual analyses below will give you an intuitive grasp of each protocol’s operational mechanics.

1. Imagine Every Stablecoin Protocol as a Bank

- Assets: The reserves held by the protocol (fiat currencies or crypto assets).

- Liabilities: The “digital dollars” issued to users.

- Equity Holders: Shareholders or token holders of the protocol, who earn fees for providing liquidity and governance.

1.1 Full‑Reserve Bank (100 % Reserve)

The left side shows physical US Dollar reserves; the right side shows the corresponding digital dollar liabilities. Each unit of liability is backed 1:1 by reserves, and when a holder redeems, the liability is burned and the physical dollar is transferred out.

This model precisely describes how fiat‑backed stablecoins such as Tether (USDT), USD Coin (USDC), and Binance USD (BUSD) operate.

In a full‑reserve bank, shareholders profit from minting and redemption fees. As long as the bank guarantees convertibility, arbitrageurs can keep the peg stable with minimal friction.

Note for U.S. users: When converting fiat to crypto or vice‑versa, use Binance.US or other U.S.–compliant platforms instead of the global Binance exchange. International transfers typically rely on SWIFT or SEPA for USD movements.

---

2. Fully‑Collateralized Crypto Stablecoins

2.1 How to Achieve a 1:1 Reserve in a Volatile Crypto Environment?

Cryptocurrencies are inherently price‑fluctuating, so a naïve 1:1 collateralization cannot guarantee the stablecoin’s value safety. The solution is over‑collateralization—the reserve’s market value must exceed the issued liability, providing a buffer against price drops.

MakerDAO follows this approach and issues DAI.

- DAI stays relatively stable because the total value of its collateral far exceeds the amount of DAI in circulation.

- For a deeper dive, see the article “What Is MakerDAO?”.

2.2 Synthetix’s sUSD

Synthetix accepts only its native token SNX as collateral. Because SNX is highly volatile, the system requires roughly 600 % over‑collateralization for every $1 of sUSD minted.

- sUSD currently trades close to $1.

- Like MakerDAO, both protocols function as full‑reserve banks that are over‑collateralized with crypto assets rather than fiat.

---

3. Algorithmic Central Bank

These stablecoins do not have redeemable reserves and lack traditional depositors; they behave more like an algorithmic central bank. Market operations and incentive mechanisms are used to keep the price anchored to the target.

3.1 Core Operational Scenarios

- Price above the peg: The system expands supply or sells reserves to push the price down.

- Price below the peg: The system buys back tokens or acquires reserves to pull the price up.

The following example uses Fei to illustrate the simplest possible model.

- Fei lost its peg immediately after launch and relies heavily on Uniswap for trading, employing “re‑weighting” and “direct incentives” to balance supply and demand.

- At present, FEI has already decoupled from $1.

3.2 Celo Dollar (cUSD)

- cUSD is primarily collateralized by CELO, while also holding a diversified basket of other crypto assets.

- When the total asset value falls below 200 % of liabilities, the protocol levies a CELO transfer fee to replenish the reserve.

- cUSD currently trades near its target exchange rate.

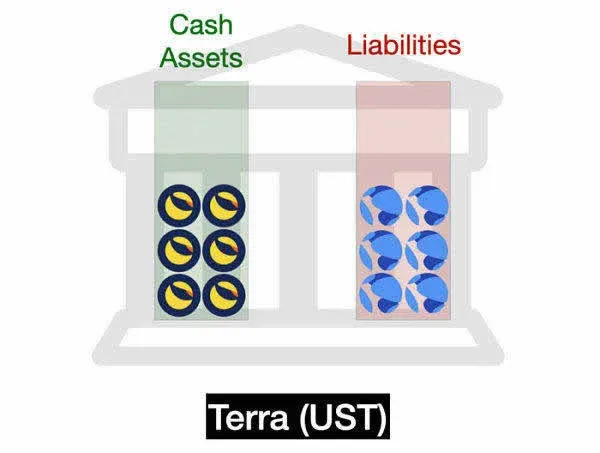

3.3 Terra UST

- UST is backed by LUNA, and the protocol itself acts as a market‑making engine. If reserves are exhausted, new LUNA is minted to rebalance the system.

- UST has recently hovered around $1 again.

Explanation: The three algorithmic stablecoins above do not provide direct redemption; instead, they rely on open‑market buying and selling to maintain price. The market‑maker’s credibility is encoded in smart contracts, effectively replicating a redeemable mechanism without holding explicit reserves.

---

4. Seigniorage Shares Model

Proposed by economist Robert Sams in 2014, this model has never been fully realized in production. Its core idea is to separate the stablecoin from bond/equity tokens, creating two independent token classes.

4.1 Basis Cash

Basis Cash is the most emblematic Seigniorage Shares project and has inspired many later algorithmic stablecoins.

- When the system’s debt is not fully repaid, it enters a contraction phase in which supply growth cannot cover outstanding obligations.

- If demand continues to rise, bonds are eventually fully redeemed, triggering an expansion phase where shareholders receive newly minted Basis Cash—the so‑called seigniorage tax.

- Unlike a traditional central bank, Basis Cash distributes the tax to shareholders instantly rather than retaining it on the balance sheet.

- Because the balance sheet holds virtually no reserves, this design is highly vulnerable to a death spiral during confidence crises; Basis Cash has already lost its peg.

Tax reminder: In many jurisdictions, any profit generated from the receipt of seigniorage tokens or from the appreciation of minted tokens may be subject to capital gains tax. Participants should consult local tax regulations.

4.2 Empty Set Dollar (ESD)

- ESD (original ESD v1) builds on the Basis Cash concept by merging “equity tokens” and the “stablecoin” into a single instrument.

- The yield generated by the collateral is re‑minted as additional ESD, causing extreme price volatility that once ranged from $0.20 to $2.00.

- ESD v1 has also lost its peg, and the development team has moved on to a brand‑new design.

To date, most pure Seigniorage Shares‑type stablecoins have ended in failure—examples include Basis, ESD, DSD, among others. This pattern underscores how subtle design choices dictate the survivability of a stablecoin system.

---

5. Closing Thoughts

In the early days of DeFi, many believed that a truly decentralized stablecoin was fundamentally impossible. In hindsight, that conclusion appears overly hasty. Each design carries its own set of advantages and risks, and there remains ample room for innovation and improvement.

Recommendation: Do not place blind trust in a project solely because its whitepaper looks impressive. Conduct your own walkthrough of the underlying mechanics and sketch out the architecture; this habit greatly deepens comprehension.

The above constitutes a visual, full‑scale analysis of stablecoins: USDT, DAI, FEI, Basis Cash, and ESD. For further related articles, follow Bitaigen (比特根).

Related Reading

- Stablecoins Explained: Mechanics, Uses & Challenges vs CBDCs

- Stablecoin Instability: USDT Supply‑Demand & Credit Risks Explained

- DeFi Revolution: Decentralized Finance Redefining Banking

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.