In the current cryptocurrency market environment, Bitcoin (BTC) and Ethereum (ETH) are falling while they fail to rise.

This is because the crypto market is in the final stage of deleveraging, with insufficient inflows of capital and amplified structural risks, making it difficult for BTC and ETH to follow the upward moves of other risk assets.

---

Bitcoin (BTC) and Ethereum (ETH) have recently underperformed other risk assets quite noticeably. We believe that the main drivers of this phenomenon include the phase of the trading cycle, market micro‑structure, and manipulation by certain exchanges, market makers, or speculative funds.

From three perspectives—late‑stage deleveraging, capital flows, and market structure—we dissect why Bitcoin and Ethereum struggle to rebound in sync during the recent downtrend. The article outlines the macro backdrop, cyclical characteristics, and reveals potential market‑maker behavior, helping readers build a clearer asset‑assessment framework. It is worth a careful read.

Market Background

- Deleveraging‑driven decline began in October of last year, hitting highly leveraged participants (especially retail traders) hard, wiping out large amounts of speculative capital and pushing the overall market toward a risk‑off stance.

- At the same time, AI‑related stocks surged aggressively in China, Japan, South Korea, and the United States, while precious metals experienced a near‑meme‑style rally fueled by FOMO (fear of missing out). These assets siphoned off a lot of retail capital.

- Crypto assets have not yet been fully integrated into the traditional financial system (TradFi); asset‑allocation switches still face regulatory, operational, and psychological hurdles.

- Professional institutional investors still represent a limited share of the crypto market. Retail participants often lack an independent analytical framework, making them vulnerable to speculative capital or market‑maker influence, which repeatedly amplifies narratives such as the “four‑year cycle” or the “Christmas curse” despite their weak logical foundations.

Traditional financial assets can be moved freely within a single account, whereas crypto assets remain subject to multiple constraints, hindering liquidity flow between markets.

The Importance of the Time Dimension

| Cycle | BTC Performance | ETH Performance | Conclusion |

|---|---|---|---|

| 3 years | Underperformed most assets | Weakest | Poor short‑term showing |

| 6 years (since 2020‑03‑12) | Outperformed most assets | Strongest | Long‑term edge emerges |

- Ignoring the underlying logic and focusing only on short‑term price swings is the most common and fatal mistake in investment analysis.

- Over a longer horizon, the current “short‑term underperformance” is merely a mean‑reversion step within the historical cycle.

Asset Rotation Is a Normal Phenomenon

- In October last year, silver experienced a short‑covering squeeze and became the worst‑performing risk asset; however, over a three‑year cycle silver has turned into the best‑performing asset.

- This rotation mirrors the situation of BTC and ETH: weak in the short run but still advantaged over a six‑year horizon.

As long as the narrative of Bitcoin as “digital gold” and a store of value remains unrefuted, and Ethereum continues to fuse with AI while serving as core infrastructure for the RWA (real‑world asset) trend, there is no rational basis to claim that they will persistently lag other assets in the long run.

Market Structure and Deleveraging

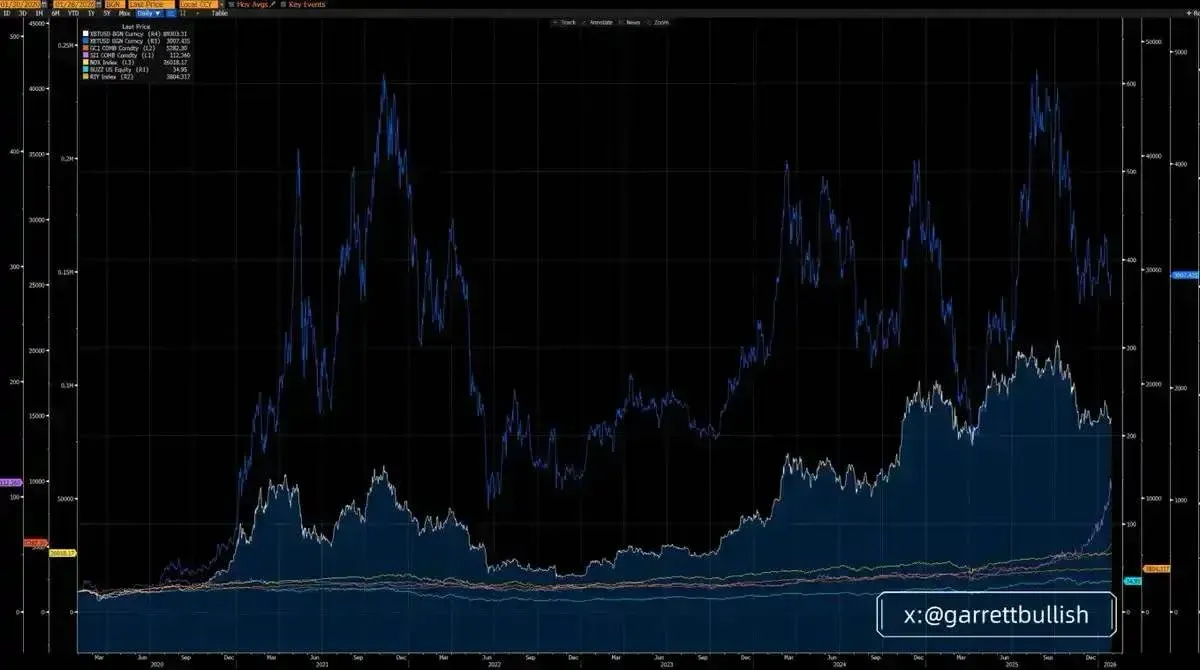

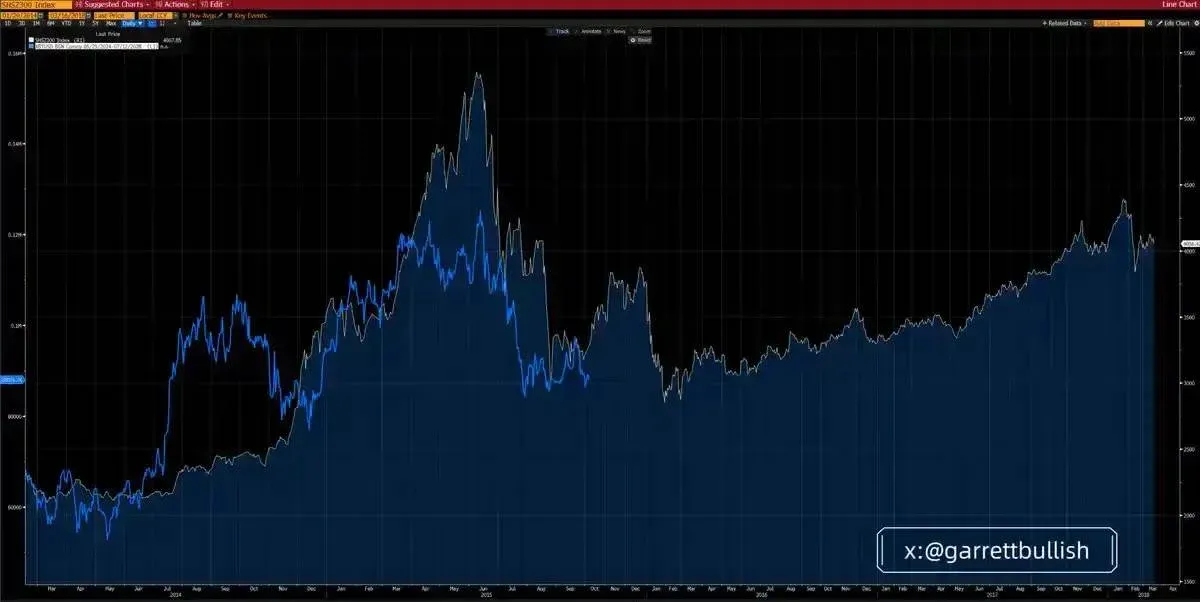

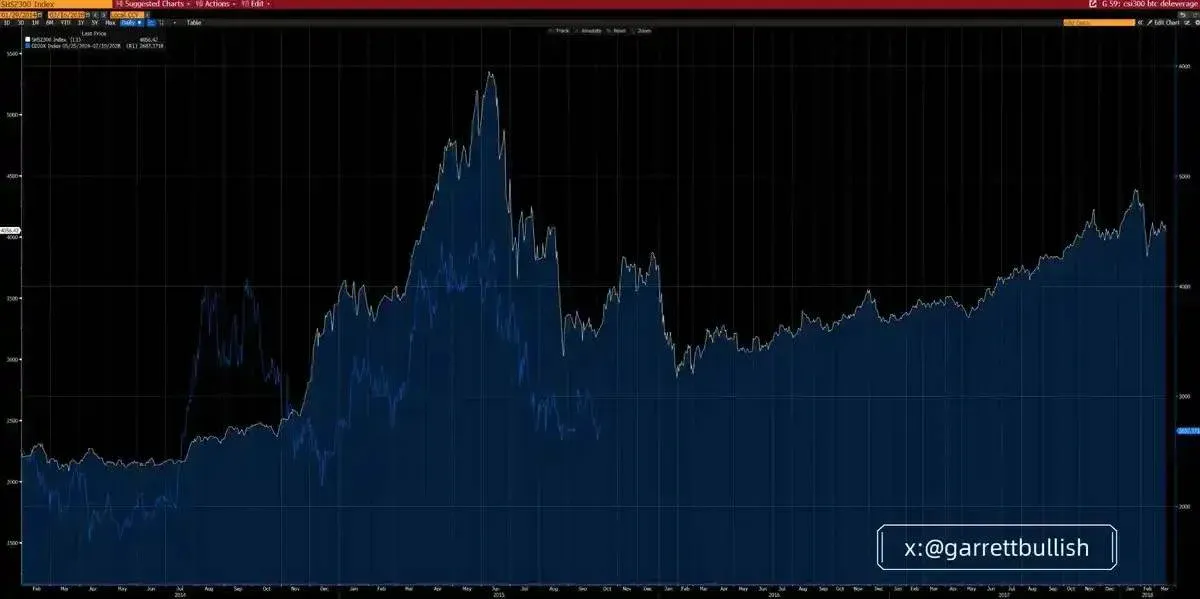

- The present crypto market bears a striking resemblance to China’s A‑share market in 2015 after a high‑leverage boom entered a deleveraging phase, both displaying a three‑stage A‑B‑C downward structure.

- Shared characteristics include: high leverage, extreme volatility, valuation‑bubble peaks, repeated deleveraging shocks, prolonged declines, volatility contraction, and a persistently positive futures‑price spread (contango).

- The positive spread translates into a discount for Digital Asset Treasury (DAT)‑related listed companies (e.g., MicroStrategy, BMNR) relative to their adjusted net asset value (mNAV).

On the macro side, regulatory certainty is strengthening (e.g., the Clarity Act), the SEC and CFTC are pushing for on‑chain trading of U.S. equities, and monetary conditions are easing—interest‑rate‑cut expectations are warming, quantitative tightening (QT) is nearing its end, share‑repurchase markets are receiving liquidity injections, and expectations of a more dovish new Federal Reserve Chair are improving the overall liquidity environment.

ETH and Tesla: A Parallel

- In 2024, Tesla’s stock price went through a head‑and‑shoulders bottom, a rebound, a consolidation, a top‑building phase, a rapid decline, and a low‑level sideways range, only to break out into a new bull market in May 2025.

- ETH’s technical pattern and fundamentals exhibit a striking similarity: it possesses both a technical narrative and meme‑driven appeal, attracting leveraged capital, experiencing sharp volatility, and then entering a deleveraging adjustment period.

As time progresses, market volatility gradually eases while fundamentals and the macro environment continue to improve.

Market Activity

- From futures trading volume, the activity levels of BTC and ETH are approaching historic lows, indicating that the deleveraging process is nearing its conclusion.

Are BTC and ETH “Risk Assets”?

- Risk assets typically exhibit high volatility and a high beta. U.S. equities, Chinese A‑shares, base metals, BTC, and ETH all meet this definition and usually benefit in a “risk‑on” environment.

- However, because of the DeFi ecosystem and on‑chain settlement mechanisms, BTC and ETH can also display safe‑haven traits similar to precious metals in certain scenarios, especially during periods of heightened geopolitical tension.

Labeling BTC and ETH simply as “pure risk assets” and then asserting that they cannot benefit from macro‑level expansion is a classic case of cherry‑picking and double standards. If a systemic risk truly existed, all risk assets would fall together; yet AI and high‑tech demand remain robust and are not significantly dampened by geopolitical noise.

The Real Underlying Causes

- Structural issues lie at the core: the crypto market is at the tail end of a deleveraging cycle, sentiment is tight, and downside risk sensitivity is high.

- The market remains retail‑dominant, with limited professional institutional participation. ETF inflows tend to reflect passive sentiment‑following rather than active, fundamentals‑driven allocation.

- DAT positioning is generally passive, often using VWAP, TWAP, or other non‑aggressive algorithms, with the primary goal of reducing intraday volatility.

- Speculative funds aim to generate intraday price swings; at the current stage, most of that volatility is downside‑biased, facilitating price manipulation.

- Retail traders commonly employ 10–20× leverage. Exchanges, market makers, or speculative funds are more inclined to profit from micro‑structure advantages rather than endure medium‑ to long‑term price risk.

- During thin‑liquidity windows (e.g., Asian overnight 00:00–08:00 UTC), concentrated sell‑offs often trigger forced liquidations, margin calls, and passive selling, magnifying the downward move.

Without fresh capital inflows or a resurgence of FOMO sentiment, the existing stock of capital alone struggles to offset the described market dynamics.

Definition of Risk Assets

Risk assets refer to financial instruments that carry a notable degree of risk, including equities, commodities, high‑yield bonds, real estate, and currencies. Their common trait is high price volatility, meaning their value can change dramatically over time.

Common Types of Risk Assets

- Equities: Prices are influenced by company performance, macro‑economic conditions, and a host of other factors, leading to sizable fluctuations.

- Commodities: Such as crude oil, gold, and agricultural products; prices are primarily driven by supply‑and‑demand dynamics.

- High‑Yield Bonds: Lower credit ratings and higher coupons come with elevated default risk.

- Real Estate: Values shift with market cycles and policy changes.

- Currencies: Forex rates react quickly to geopolitical events, macro data releases, and monetary‑policy moves.

Main Characteristics of Risk Assets

- Volatility: Prices swing frequently, offering both profit opportunities and loss potential.

- Reward‑Risk Trade‑off: Higher risk can bring higher expected returns, but also a greater chance of loss.

- Sensitivity to Market Environment: They react strongly to interest rates, economic indicators, investor sentiment, and other macro variables.

---

In summary, this article has examined why Bitcoin and Ethereum tend to fall together rather than rise together. For more Bitcoin‑price‑related content, please search for previous Bitaigen (比特根) articles or continue browsing the related posts below. We appreciate your continued interest and support for Bitaigen (比特根)!

Note for U.S. readers: When accessing cryptocurrency exchanges, use Binance.US rather than the global Binance platform.

Tax disclaimer: Cryptocurrency gains may be taxable in your jurisdiction; please consult a local tax professional for guidance.

Related Reading

- Bitcoin Whales Add 236K BTC in V‑Shaped Bottom‑Fishing

- Bitcoin Weekly RSI Near Historic Lows, Liquidity Battle

- Bitcoin Enters Early Bear Market; $84K Support Crucial

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.