We dissect the recent dramatic volatility of Bitcoin from two perspectives—the ETF structure and secondary‑market trading activity—to uncover the true drivers behind the price swings and to clarify the distinction between IBIT’s settlement path and the settlement of Bitcoin itself. This article will help readers rationally evaluate the media focus, gain a deeper understanding of the market‑impact transmission mechanism, and avoid misinterpretation.

Key Takeaways

- On the same day that Bitcoin fell sharply on 5 February, IBIT’s secondary‑market trading volume hit an all‑time high, but the activity was a net creation rather than the traditional net redemption.

- Although secondary‑market trading was unusually vigorous, the actual amount of Bitcoin redeemed in the primary market remained limited.

- Price pressure was mainly transmitted to Bitcoin through hedging actions taken by authorized participants (APs) in the spot or futures markets.

- It is essential to differentiate IBIT’s secondary‑market settlement (which only involves ETF shares) from the settlement of Bitcoin itself; the two‑tier ETF structure creates distinct impact pathways.

---

How the Market Narrative Forms

Whenever a sharp price decline occurs, public discourse quickly seeks a “culprit.” The recent plunge on 5 February, followed by an almost $10,000 rebound the next day, sparked extensive debate. Jeff Park, a Bitwise consultant and Chief Investment Officer at ProCap, argued that this volatility is more tightly linked to the internal mechanics of the Bitcoin spot‑ETF ecosystem than external observers assume, with the key clue residing in the secondary market of BlackRock’s iShares Bitcoin Trust (IBIT) and its options segment.

IBIT’s Unusual Performance on the Day

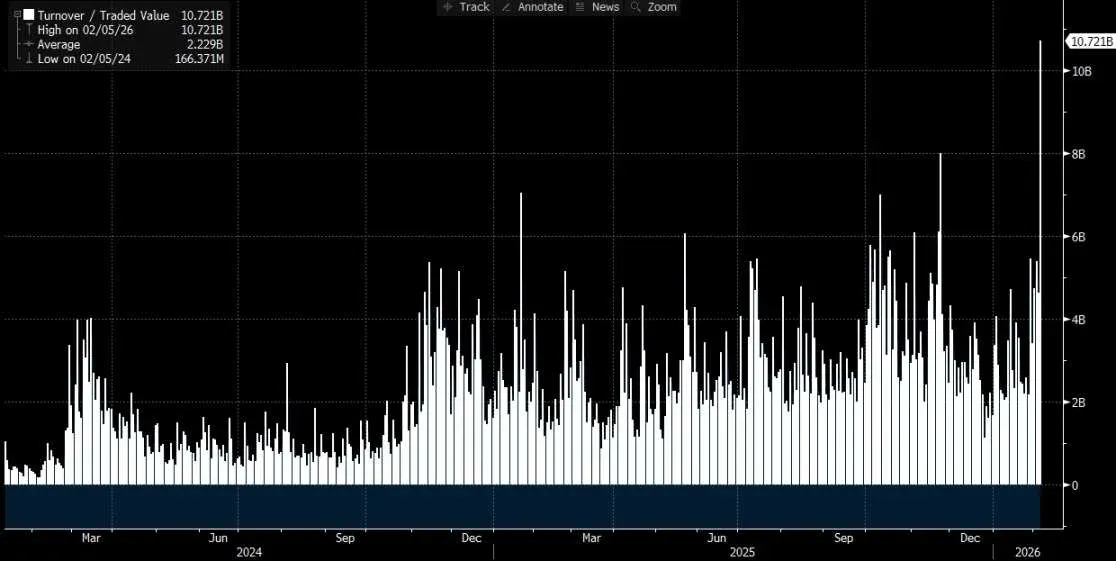

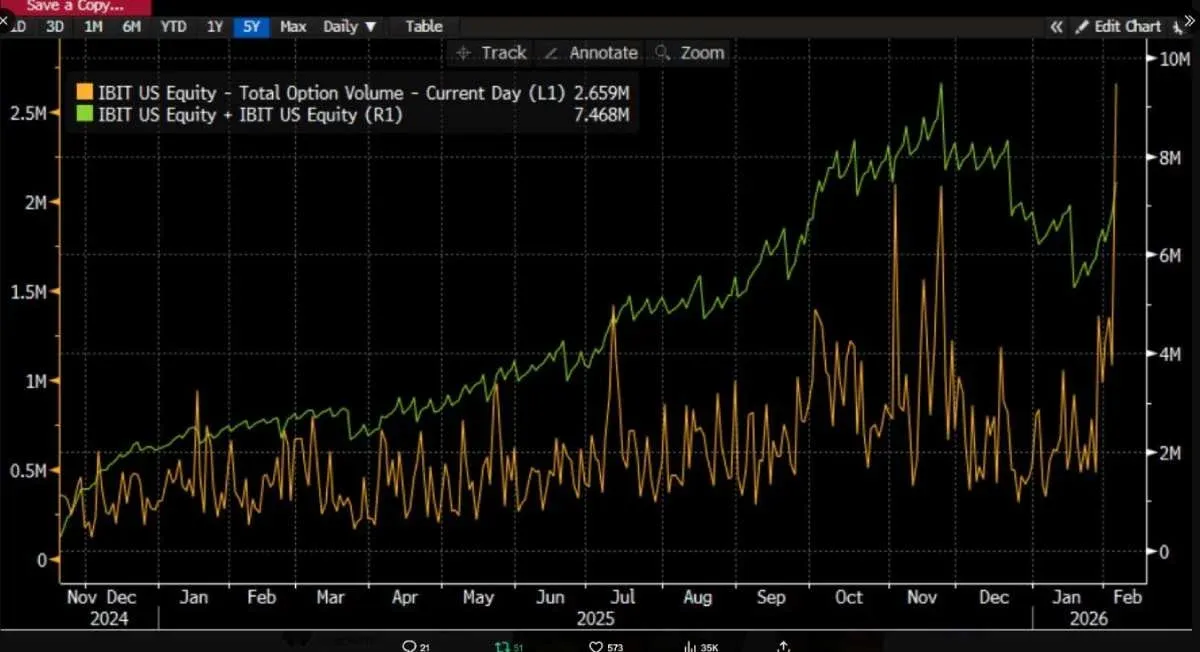

Jeff Park pointed out that on 5 February, both IBIT’s trading turnover and its options volume shattered historical records, with the options skewed toward bearish strikes. More surprising was the fact that, contrary to past experience where double‑digit daily price drops usually trigger pronounced net redemptions and capital outflows from an ETF, IBIT recorded a net creation. The influx of new shares expanded the overall size of the spot‑ETF, resulting in a net inflow of capital.

This “sharp drop accompanied by net creation” undermines the simplistic explanation that “ETF investors panic‑redeem, pushing the price down.” Instead, it aligns with the conventional deleveraging and risk‑reduction process within the broader financial system: market makers, dealers, and multi‑asset portfolios are forced to trim exposure under derivative‑based hedging frameworks, and the selling pressure originates from the adjustment of paper‑based balance‑sheet positions and the compression of hedging chains. The pressure is ultimately transmitted to Bitcoin prices through IBIT’s secondary‑market trades and options hedges.

The Causal Chain That Needs Clarification

Many commentators equate the institutional settlement of IBIT with the Bitcoin crash, but without unpacking the ETF mechanics this causal link is easily mis‑ordered. Secondary‑market transactions involve ETF shares themselves; the factor that truly influences the custodial layer of Bitcoin is the primary‑market creation and redemption process. Mapping secondary‑market volume linearly onto an equal amount of spot‑market sell‑offs ignores several critical steps and is therefore logically unsound.

What Does “IBIT Triggers Massive Settlement” Actually Mean?

The controversy surrounding IBIT centers on which market tier and which mechanism ultimately impact BTC pricing. The most common narrative focuses on primary‑market net outflows: if ETF investors panic‑redeem, authorized participants (APs) must sell the corresponding Bitcoin to meet redemption obligations, injecting selling pressure into the spot market and causing price declines and liquidations.

However, this intuition overlooks a key fact: ordinary investors and most institutions cannot directly create or redeem ETF shares in the primary market; only entities with special AP credentials can perform those operations. The “daily net inflow/outflow” figures that appear in reports refer to changes in the total number of primary‑market shares, while secondary‑market trades merely shift ownership of existing shares and do not directly alter the custodial Bitcoin balance.

Analyst Phyrex Ni further clarified that the “settlement” Parker mentions actually pertains to the settlement of the IBIT spot‑ETF itself, not to the settlement of Bitcoin. In the secondary market, participants trade the IBIT “ticket,” whose price is anchored to BTC, but the transaction occurs entirely within the securities market and does not move the underlying asset.

The Real Flow in the Primary Market

The only channel that can directly affect Bitcoin is the creation and redemption process in the primary market, which is executed by APs (effectively market makers). When creating new shares, an AP must deliver the requisite Bitcoin or cash consideration; the supplied Bitcoin enters the custodial pool and is subject to regulatory constraints, meaning the issuer and its partners cannot freely reallocate it. During redemption, the custodian transfers Bitcoin to the AP, which then handles downstream disposal and cash settlement.

An ETF operates as a two‑tier system: the primary market handles the actual buying and redeeming of Bitcoin, with liquidity provided almost exclusively by APs; the secondary market facilitates the buying and selling of ETF shares, akin to trading ordinary equities on a stock exchange. Even in the event of a large‑scale redemption, an AP does not necessarily have to sell Bitcoin on a public spot exchange. It may draw from its own inventory or, within the T+1 settlement window, employ more flexible delivery mechanisms. Consequently, in the so‑called “massive settlement” on 5 January, BlackRock investors actually redeemed fewer than 3,000 BTC, and the combined redemption across all U.S. spot‑ETF providers did not exceed 6,000 BTC—far below the secondary‑market turnover figures.

It is noteworthy that Parker cited an IBIT secondary‑market turnover of roughly $10.7 billion USD, a historical peak. This figure reflects only the exchange of ETF shares and does not necessarily translate into Bitcoin movement on the primary market. In other words, IBIT’s secondary‑market settlement is not synonymous with Bitcoin’s settlement.

From Secondary‑Market Activity to Spot‑Market Impact

When long positions in IBIT are forced to unwind in the secondary market and buying demand cannot absorb the sell‑off, IBIT’s market price may trade at a discount to its net asset value (NAV). As the discount widens, arbitrage opportunities expand, prompting professional market makers and arbitrageurs to purchase discounted IBIT shares to capture the spread. This process by itself does not directly generate spot‑market selling pressure on Bitcoin.

Nevertheless, once an AP acquires discounted IBIT shares, it typically needs to hedge the resulting net exposure promptly. Hedging can be executed by selling the underlying Bitcoin in the spot market or by opening short positions in Bitcoin futures. If the AP opts for spot sales, the pressure is transmitted immediately to Bitcoin prices; if it chooses futures shorts, the initial effect appears as a basis change, which later influences the spot market through cross‑market arbitrage or quantitative trading strategies.

After completing the hedge, the AP’s overall position becomes relatively neutral, allowing it to decide when to dispose of the IBIT shares. One approach is to redeem the shares with the issuer on the same day, which would appear in official flow data as a net redemption. Another approach is to hold the shares, wait for secondary‑market sentiment to improve or for the price to rebound, and then sell the shares on the secondary market, thereby completing the entire trade without ever entering the primary market. If the next day IBIT’s price re‑establishes a premium or the discount narrows, the AP can realize a spread profit in the secondary market while simultaneously closing the previously opened futures short or replenishing any spot inventory that had been sold.

Even when the final disposal of shares occurs primarily in the secondary market, primary‑market net redemptions may remain minimal. Yet the AP’s hedging actions in the spot or futures arena can be sufficient to spill over the secondary‑market pressure into the Bitcoin market, forming an indirect transmission chain.

Closing Remarks

In summary, the sharp decline of Bitcoin on 5 February was not caused directly by a secondary‑market settlement of IBIT. Instead, the impact was conveyed indirectly through the hedging activities of authorized participants in the spot or futures markets. The ETF’s two‑tier architecture means that secondary‑market volume does not equate to actual Bitcoin sales; the primary‑market creation/redemption process and the associated hedging behavior remain the true drivers of spot‑price movements. Although the net outflow from Bitcoin spot ETFs on that day represented only 0.46 % of total holdings (1,273,280 BTC total, net outflow 5,952 BTC), the amplification effect of the hedging chain still produced a price drop exceeding 14 %.

For readers who wish to explore the specific role of IBIT in Bitcoin’s price crash further, you may search for prior analysis articles from Bitaigen (比特根) or continue reading the linked resources below. Thank you for following and supporting Bitaigen.

*All fiat‑currency references are expressed in United States dollars (USD). Transactions can be settled via SEPA or SWIFT where applicable. U.S. residents should use Binance.US rather than the global Binance platform. Please note that gains from cryptocurrency transactions may be subject to taxation under the laws of your local jurisdiction.*

Related Reading

- Bitcoin Whale Buys 40,000 BTC, Sparkling $70,000 Price Rebound

- Bitcoin Spot ETFs Face $200M Outflows Amid Bullish Push

- Bitcoin & Ethereum ETFs Lose $1B, Market Down 6%

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.