By closely dissecting Ethena’s recent capital deployment and derivatives data, we expose a shift in risk appetite across the crypto market and the subtle signals in liquidity supply‑and‑demand. This article will help readers identify a possible inflection point and gain a deeper understanding of the macro forces at play, and is worth a thorough read.

Market Overview and Ethena’s Capital Deployment

In the past several months the crypto‑asset universe has displayed a pronounced risk‑off sentiment. To capture a potential turning point, I have been continuously monitoring a variety of derivatives metrics and, together with Ethena’s publicly‑available transparency dashboard, analysing the market’s risk appetite.

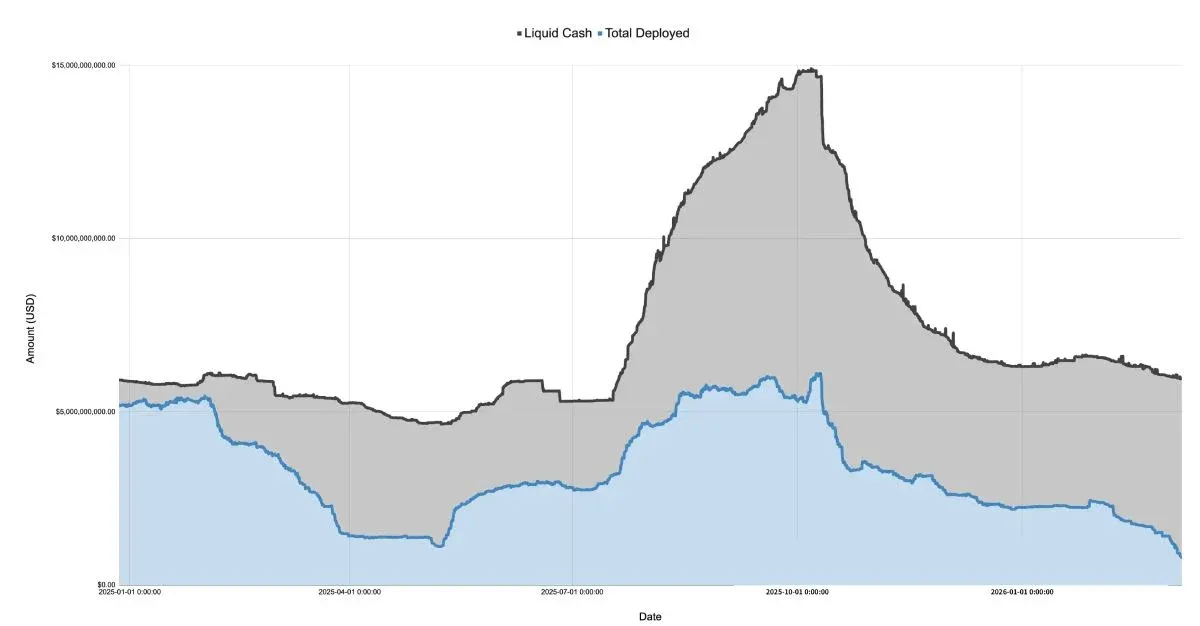

From the balance‑sheet snapshot covering 2024‑12‑27 to 2026‑03‑07, we can see that the capital Ethena has deployed has slipped to only 71 % of its 2025 low‑point level. This is not a criticism of the project itself, but rather a reflection of the current overall demand.

*(Figure: Ethena Balance Sheet 2024‑2026)*

Correspondingly, the deployment size has fallen sharply from the rapid risk‑avoidance phase that followed the $TRUMP token launch in January 2025. Capital that once exceeded $5 billion has contracted to roughly $1.108 billion, a decline of more than 75 %.

It is worth noting that Ethena’s deployed capital is often treated as a barometer for whether long‑side demand is outstripping supply. While Ethena is not the sole basis‑trade entity, its scale typically represents about 25 % of the combined volume on Binance and Bybit. Whenever it holds ample cash, it will enlarge its positions to fill unmet long‑side demand. Consequently, even if the overall long‑side demand in April 2025 did not drop by a full 75 %, the excess demand that was being absorbed by targeted short‑covering has shrunk by a comparable magnitude.

Note for U.S. readers: When the article mentions Binance, U.S. users should access the platform via Binance.US rather than the global Binance site.

Perpetual Contracts Structure and Matching Mechanism

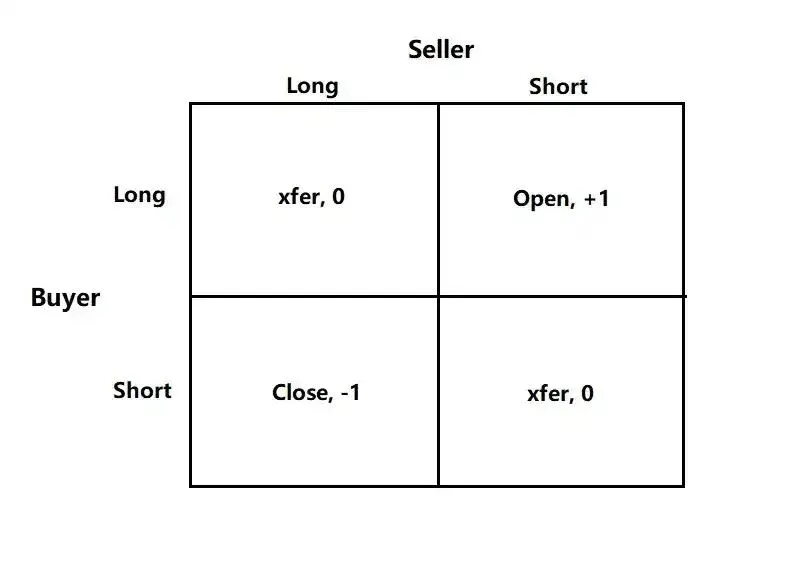

Since BitMEX introduced a 100×‑leverage product, perpetual contracts have become the highest‑volume trading segment in crypto, with daily turnover often 5‑20 times that of spot markets. Their core characteristic is a 1:1 long‑short correspondence: every long contract is obligatorily matched by an equal‑sized short contract. Exchanges act as match‑makers, ensuring that each contract always has a counterpart on the opposite side.

The table below illustrates the four possible matching outcomes that can occur on an exchange.

Perpetual‑Contract Matching Matrix

- If both counterparties are long (or both short), the exchange merely transfers ownership; no new contracts are created or destroyed.

- When the buyer goes long and the seller goes short, a new contract must be minted, increasing open interest by one unit.

- Conversely, if the buyer goes short and the seller goes long, the exchange can directly offset and delete the corresponding contract, decreasing open interest by one unit.

Participant Profiles

Based on trading motives, holders of perpetual contracts can be broadly grouped into four categories:

- Directional Longs – risk‑takers seeking net exposure.

- Directional Shorts / Hedgers

- a. Direct short positions on assets or hedging activities;

- b. Use of structured products for hedging.

- Basis Traders (e.g., Ethena) – provide excess short liquidity when supply‑and‑demand become imbalanced.

- Hybrid Arbitrageurs – simultaneously hold long and short positions to capture tiny price differentials at near‑zero cost.

Directional shorts include investors willing to bear downside on assets as well as institutions that short to reduce tax liabilities. Venture‑capital firms, employee teams compensated with tokens, and similar entities often short liquid assets such as Bitcoin or Ethereum to hedge holdings in illiquid projects (e.g., Monad). Projects like Neutrl adopt comparable tactics, treating hedging as a source of revenue.

Basis traders, on the other hand, are indifferent to directional risk; they simply exploit supply‑and‑demand mismatches by supplying short liquidity whenever long demand exceeds the available short supply. Their position sizes are typically highly elastic.

Arbitrageurs work to flatten minor price gaps between different perpetual contracts, incurring only transaction fees; consequently, their long and short holdings remain perfectly offset.

From the above structure we can derive the following identity:

Directional Long + Arbitrage Long = Directional Short + Basis Short + Arbitrage Short

Because arbitrage longs and arbitrage shorts cancel each other out, the equation simplifies to

Directional Long = Directional Short + Basis Short

This is precisely the rationale behind Ethena’s “basis‑short” proxy metric.

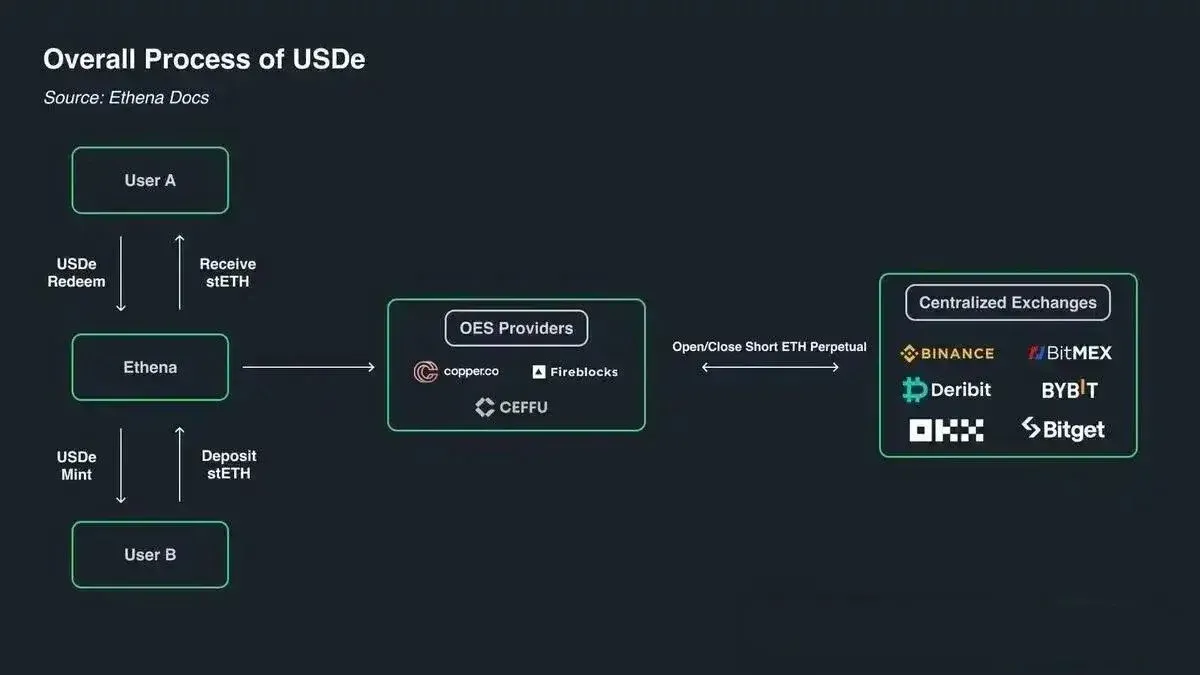

Ethena Mechanism Diagram

Ethena’s core business is to act as the counter‑party for leveraged long traders, providing short‑side funding. When a trader wishes to go long on a perpetual contract but lacks capital, they borrow the equivalent amount from Ethena and pay a basis spread plus financing fees.

*(Figure: Ethena Mechanism Overview)*

Capital Changes and Their Relationship to Bitcoin Price Movements

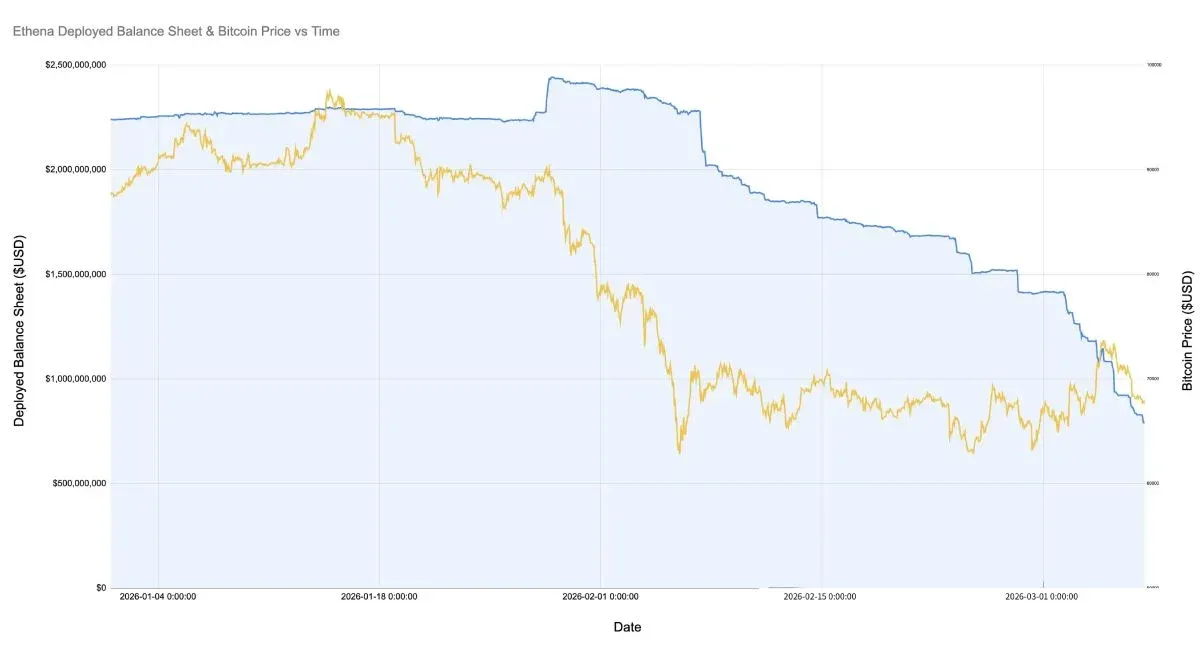

As of 2026‑02‑08, Ethena’s cumulative deployment across all major markets (BTC, ETH, SOL, BNB, XRP, HYPE) totals roughly $791 million, which is only 71 % of its 2025 trough and merely 12.9 % of the peak observed before 2025‑10‑10. This figure is not a condemnation of Ethena; rather, it mirrors the fact that net long demand is currently at a historic low.

During Bitcoin’s sharp decline to $60,000, Ethena had allocated more than $2 billion in basis positions. Since 2026‑02‑08, that amount has contracted by about 60 %.

*(Figure: Ethena Deployed Capital vs. Bitcoin Price 2026)*

The primary drivers behind the rapid shrinkage of basis positions are:

- The unwinding of profitable yet unsustainable basis trades that emerged after February;

- Heightened activity from directional shorts and hedgers, which squeezed the space available to opportunistic basis traders;

- A shortage of leveraged long demand.

Looking at total open interest, contracts on Bitcoin and other leading coins have remained relatively stable, yet funding rates have stayed negative for an extended period. SOL, in particular, shows negative cumulative funding across multiple exchanges, indicating rising demand for short or hedge positions.

*(Figure: Open Interest and Funding Rate Trends)*

Potential Shifts in Market Structure

The most striking current observation is that the scale of directional longs and directional shorts is almost equal—a rarity in crypto history. While there is not yet sufficient evidence to claim that this equilibrium will become a long‑term norm, nor to assert that existing market mechanisms must be rewritten, the near‑symmetry is nevertheless anomalous when compared with traditional asset classes.

From the perspective of small‑ and mid‑cap projects, entities such as Eigen, Grass, Monad, and others are often backed by dozens of venture‑capital firms and cash‑flow‑positive operating companies. When these backers need to lock in profits or limit losses, they frequently turn to structured products for “relatively crowded” hedging trades—essentially shorting a basket of correlated assets.

We observed heightened activity of such structured products during the rapid rally of Ethereum (ETH), followed by a wave of short‑covering across numerous mid‑cap tokens. At the same time, opportunistic basis traders like Ethena were noticeably pushed out of the market.

Conclusion

In summary, the evolution of Ethena’s capital deployment reveals a delicate balance between long and short forces in today’s crypto market, alongside an uptick in hedging demand. Should this balance persist, it may signal that market risk appetite is moving toward a relatively steady state. For readers seeking deeper analysis of Ethena’s trajectory and broader market risk sentiment, please refer to prior articles from Bitaigen (比特根) or continue exploring the related links below. Stay informed, and together let’s navigate the future of the crypto space!

Tax Disclaimer: Crypto‑related gains may be taxable in your jurisdiction. Please consult a qualified tax professional and consider local regulations when handling crypto transactions.

---

*All fiat references in this translation use U.S. Dollar (USD). For cross‑border transfers, SEPA (Euro) or SWIFT (global) payment networks are commonly employed.*

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.

⚠️ Risk Disclaimer: Crypto prices are highly volatile. This is not investment advice.