In this article we outline the compliance requirements set out by the GENIUS Act for U.S. payment‑stablecoins, focusing on which tokens already meet the new regulations and may therefore enjoy broader application in a compliant environment, while also highlighting projects that still face risks. To learn more about the details of the legislation and its impact on token holders, keep reading.

Which stablecoins stand to benefit from the GENIUS Act?

The GENIUS Act establishes a unified regulatory standard for payment‑stablecoins in the United States; only tokens that satisfy these new rules will be allowed to continue circulating in the U.S. market. The stablecoins listed below have already met the statutory requirements and are expected to gain a larger usage footprint within a compliant framework:

- USDC (Circle): Fully satisfies the Federal Reserve’s reserve‑backing criteria and retains its core role within the settlement systems of large financial institutions.

- PYUSD (PayPal): Leveraging its deep penetration in retail payment scenarios and the Act’s strengthened holder‑protection provisions, it is poised to earn greater trust in everyday e‑commerce transactions.

- USAT (Tether): After obtaining federal regulatory approval, the previously restricted issuer can now operate legally in the U.S. market.

- RLUSD (Ripple): Focused on institutional liquidity, it uses the clear legal definition to achieve compliant cross‑border payments.

- FIDD (Fidelity): As Fidelity’s digital dollar, it benefits from the provision that excludes payment‑stablecoins from securities regulation.

- USDP (Paxos): Built on a regulated trust structure, it maintains a strict 1:1 reserve ratio and undergoes monthly audits, complying with all new requirements.

By contrast, the original USDT and certain algorithmic tokens fail to meet the “1‑to‑1, short‑term Treasury” reserve structure and therefore face the risk of being delisted from U.S. platforms.

---

What does the GENIUS Act mean for investors?

The legislation mandates a 1‑to‑1 reserve, monthly audits, and a priority claim on assets in the event of bankruptcy, dramatically reducing the likelihood that ordinary holders will encounter a “run” or lose access to their assets. Investors do not need to initiate legal action; they simply need to verify that the token they hold is issued by an approved institution. Doing so allows them to enjoy more reliable asset security with compliant products such as USDC, PYUSD, and others.

Note: Crypto gains may be subject to tax in the holder’s local jurisdiction; consult a tax professional for advice.

---

Impact of the GENIUS Act on cryptocurrency exchanges

U.S.‑based exchanges (e.g., Coinbase, Kraken) must re‑evaluate the dollar‑denominated tokens they list to ensure they originate only from approved issuers. Gemini has already used this regulatory clarity to promote compliant assets, while tokens that do not satisfy the new standards face mandatory delisting.

Off‑shore platforms (such as Binance and Bybit) wishing to continue serving U.S. customers must likewise demonstrate that their technology and compliance processes meet U.S. regulatory expectations. Decentralized protocols (Uniswap, Aave) enjoy a code‑level exemption, but any profit‑generating interfaces they provide must still adhere to the service‑provider definitions of compliance to avoid potential penalties.

*U.S. users who want to trade on Binance must use Binance.US, the separate entity that complies with U.S. regulations.*

---

Key provisions of the GENIUS Act – a quick overview

Dual‑track regulation and issuance thresholds

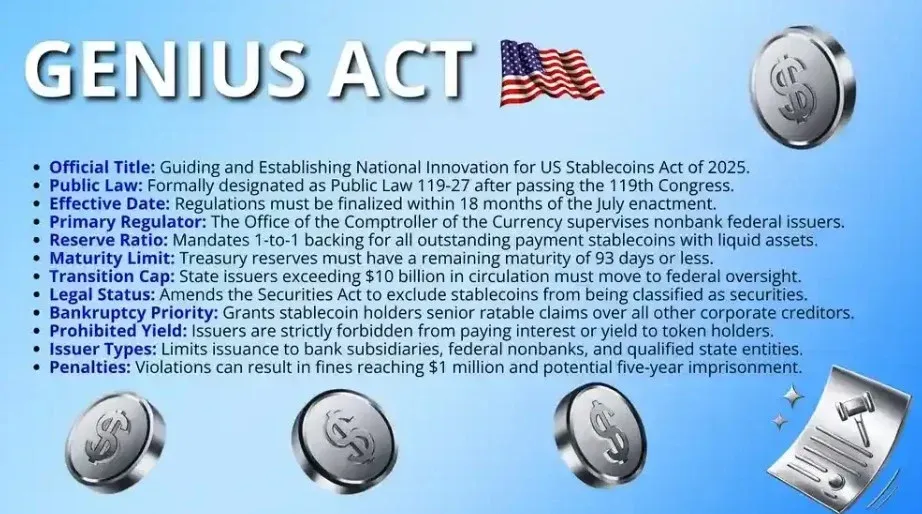

The Act creates a “dual‑track” supervisory system spanning state and federal levels, permitting only “approved payment‑stablecoin issuers” to create USD‑pegged tokens. Eligible issuers include bank subsidiaries, non‑bank entities approved by the Office of the Comptroller of the Currency (OCC), and issuers holding state‑level qualifications.

- $10 billion threshold: If a state‑regulated entity’s circulating volume exceeds $10 billion, it must transition to unified federal oversight to prevent systemic risk from spreading.

Reserve and liquidity requirements

- Qualified assets: Reserves may consist solely of U.S. coins, paper currency, or Treasury securities with a remaining maturity of no more than 93 days.

- Monthly certification: The chief executive of the issuing entity must submit a written attestation each month, mirroring the accountability mechanisms found in the Sarbanes‑Oxley Act.

- Prohibition on pledging: Reserve assets cannot be pledged or otherwise invested, ensuring they remain fully available when users redeem their tokens.

Legal classification certainty

By amending the Securities Act of 1933 and the Commodity Exchange Act, the legislation removes payment‑stablecoins from the definition of securities or commodities, allowing them to focus exclusively on payment functions without the need to register with the SEC. This provides traditional banks with a clear legal pathway to incorporate digital assets into existing payment infrastructures.

Consumer protection and bankruptcy priority

- Priority claim: In the event of issuer bankruptcy, token holders enjoy a proportional priority claim on the reserve assets.

- Expedited distribution: Courts must initiate the distribution of funds to holders within 14 days after the first hearing.

- Asset segregation: Statutory reserves are excluded from the issuer’s general assets, preventing them from being used to satisfy other corporate debts.

---

Legislative timeline for the GENIUS Act

- 2025‑05‑01 – Senator Hagerty introduces the bill.

- 2025‑05‑19 – Motion to close debate passes with 66 votes in favor and 32 against.

- 2025‑06‑17 – Senate adopts the final text (including amendments) with 68 votes for and 30 against.

- 2025‑07‑17 – House of Representatives approves the measure 308‑122.

- 2025‑07‑18 – President signs; the Act becomes public law 119‑27.

- 2025‑09‑06 – An alternative amendment is proposed to further refine the regulatory scope.

---

Definition of “stablecoin” under the GENIUS Act

For the first time, U.S. legislation provides a comprehensive statutory definition of a “payment stablecoin,” separating it from traditional investment contracts and emphasizing its utilitarian function rather than speculative nature. This definition draws a clear regulatory boundary for digital assets pegged to the U.S. dollar, eliminating years of uncertainty about token classification.

---

Pros and cons of the GENIUS Act

| **Advantages** | **Disadvantages** |

|---|---|

| **Legal certainty** – Clearly excludes compliant stablecoins from securities and commodity regulation, removing ambiguity. | **Operational burden** – Smaller firms must shoulder monthly audit costs and meet the **$10 billion** federal oversight threshold. |

| **Bankruptcy rights** – Holders receive priority claims in insolvency, safeguarding asset safety. | **Yield restrictions** – Issuers are prohibited from paying interest or other returns to holders, limiting integration with DeFi yield products. |

| **Reserve safety** – Mandatory use of highly liquid assets (e.g., ≤93‑day Treasuries) ensures a 1:1 asset‑backed structure. | **Privacy concerns** – Strict AML/KYC requirements and compliance‑technology mandates may affect user anonymity. |

---

What is the GENIUS Act?

The Guidance and Establishment of a National Innovation Framework for U.S. Stablecoins (GENIUS) Act creates a nationwide, uniform regulatory framework for payment‑type stablecoins. It obliges all issuers to maintain a 1:1 reserve backed by short‑term Treasury securities or other high‑liquidity assets, and it delineates the supervisory responsibilities of the Federal Reserve and the OCC. Simultaneously, the Act removes regulated payment stablecoins from existing federal securities or commodity laws, laying the legal groundwork for digital assets to enter the traditional U.S. financial system.

---

Final thoughts

The GENIUS Act represents a pivotal step toward bridging the conventional banking sector with the fast‑moving domestic digital‑asset market. By eliminating regulatory overlap and providing a clear compliance pathway, it opens the door to widespread institutional adoption and complements the CLEAR Act with necessary safeguards. Lawmakers have constructed essential protection mechanisms that preserve the United States’ global leadership in finance while delivering a safe, stable operating environment for every dollar‑pegged innovation.

This article offers a systematic overview of the GENIUS Act and its implications for stablecoins. For further details, search for previous Bitaigen (比特根) articles or continue browsing the related content below. Thank you for your attention and support!

Related Reading

- GENIUS Act Passed: US House Sets Federal Stablecoin Rules

- USDC vs USDT 2026: Risk Exposure, Regulation & Market Outlook

- Lagarde's ECB Exit: What the Next Governor Means for Crypto Regulation

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.

⚠️ Risk Disclaimer: Crypto prices are highly volatile. This is not investment advice.