We have organized the latest developments in the restaking ecosystem for 2024 in this article, analyzing core protocols, liquidity restaking, and the evolution of Bitcoin cross‑chain security. By deeply dissecting technical bottlenecks and the competitive landscape, we aim to help readers grasp industry pulse, spot potential opportunities, and provide practical points of focus for investment and R&D decision‑making.

1. Article Summary

- Restaking first entered mainstream attention at the DevConnect 2023 conference, and its adoption rate has since grown exponentially. Since then, restaking has evolved from a single project—EigenLayer—into a full‑stack ecosystem comprising multiple platform providers, operators, liquidity‑restaking protocols, and multi‑chain security experts.

- Although restaking remains an emerging primitive, its second‑order effects, market trajectory, and possible technical constraints merit continuous community monitoring. The competitive picture is no longer “one dominant player.” Core protocols such as EigenLayer, Symbiotic, Babylon, Jito, and a variety of liquidity‑restaking protocols and DeFi derivatives each bring distinct strengths.

- Liquidity‑restaking protocols (LRT) are often mistakenly conflated with liquid‑staking tokens (LST), yet their risk profiles are fundamentally different. LSTs only bear the homogeneous risk of the underlying asset (e.g., ETH). LRTs must simultaneously manage multiple heterogeneous risks, including inflation, slashing, and technical vulnerabilities of a specific AVS, and they support a range of collateral types and settlement currencies.

- 2024 is viewed as a pivotal year for a Bitcoin resurgence. Several teams are helping BTC holders extend Bitcoin’s economic security to other chains without relying on centralized bridges or trusted third parties. Babylon leads this direction with its technical edge, and an emerging ecosystem around it includes Lombard, Solv Protocol, PumpBTC, and other new Bitcoin liquidity‑staking projects.

- Driven by Ethereum’s broad adoption, Solana’s staking market remains relatively low‑key but is progressing steadily under new conceptual frameworks. Jito Network leads Solana’s restaking space, while Solayer, Cambrian, Picasso and others are building complementary shared‑security solutions that fill gaps in Solana’s native protocol decentralization journey.

- Oracles play multi‑layered roles in the restaking architecture: they are core components of platform design and also satisfy the need for precise pricing of novel restaked assets. Oracle networks also enable innovative shared‑security use cases, such as increasing data‑operation costs to boost network resilience, or constructing brand‑new pricing models on cost‑effective restaking availability layers.

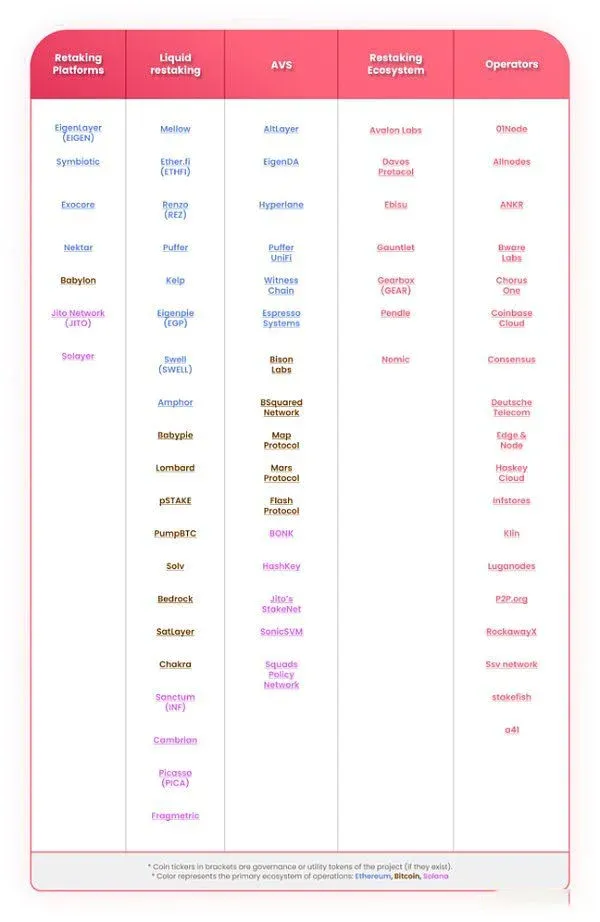

Major Projects and Institutions (see diagram below)

---

2. Restaking Overview

EigenLayer: The Trailblazer of Restaking

Since launching its deposit function in June 2023, EigenLayer has secured a solid place in the public eye, commanding roughly one‑third of Ethereum’s total value‑locked (TVL). Its core proposition is a bilateral decentralized trust market that splits and redeploys the trust layer atop Ethereum.

- Demand side – Active Validation Services (AVS). These systems perform their own validation and submit security requirements to the EigenLayer market, covering sidechains, data‑availability layers, new virtual machines, keepers, oracles, bridges, threshold encryption, and trusted execution environments. Notable examples include EigenDA, Witness Chain, and RedStone Oracles.

- Supply side – Restakers. These are users who hold ETH and stake it either via an LST or through permissionless support for any ERC‑20 token. They delegate ETH security to EigenLayer’s smart contracts, earning extra rewards while extending that security to additional networks.

In 2024, EigenLayer hit several milestones: a US $100 million Series B, the acquisition of Rio Network, the launch of the EIGEN token based on the *stakedrop* concept with transferability, the formation of an independent Eigen Foundation, the mainnet rollout of EigenDA (10 MB/s throughput), AVS mainnet rewards, a Programmatic Incentives reward scheme, a revamped slashing design, and ongoing governance enhancements.

(1) Symbiotic’s Restaking Journey

Symbiotic launched at the start of 2024, quickly gaining attention with its positioning as the “Uniswap of the restaking space.” Backed by a seed round from Paradigm and public endorsement from Lido’s founder, its deposits hit the cap on day one and grew to roughly US $17 billion TVL within a few months.

Its innovation lies in a modular, customizable design:

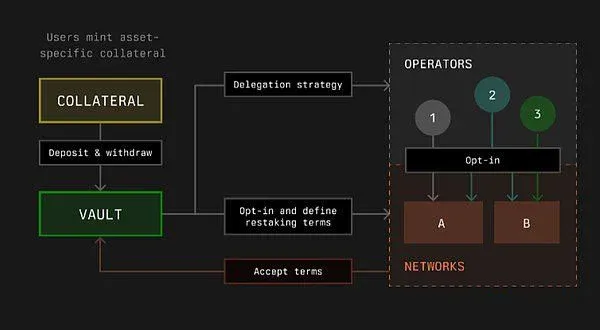

- Restakers may use any asset besides ETH and delegate security to a trust‑less Vault. Vault parameters are set once and immutable, guaranteeing long‑term term stability. Symbiotic also issues an ERC‑20 token representing each Vault’s share.

- Networks (AVS) can select reputable operators based on reputation or other metrics, flexibly configuring collateral, node operators, reward, and slashing rules, thereby achieving fine‑grained management of the security pool.

- Operators aggregate assets from many Restakers to provide security without building full infrastructure themselves, lowering both technical and economic barriers.

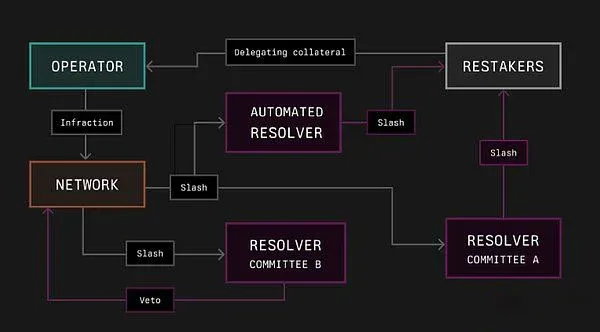

Symbiotic also introduced Resolvers, granting veto power in slashing disputes and enabling integration with oracle‑based dispute solutions such as RedStone Oracles.

A partnership with Mellow Protocol further expands permissionless LRT creation, allowing users to opt into multi‑chain shared‑security networks without bearing a single point of risk. Mellow currently locks about US $7 billion—roughly half of Symbiotic’s TVL.

Symbiotic recently announced 40 partners, including Ethena, Frax, Etherfi, and RedStone Oracles, and highlighted three support pillars: a USD‑denominated oracle price feed, exploration of RedStone’s data‑aggregation network, and provisioning of data feeds for other chains on its platform.

(2) Liquidity‑Restaking Protocols: The Fundamental Difference Between LRT and LST

At first glance, both LRT and LST let users deposit ETH (or derivatives) and outsource validation duties to professional entities while retaining most validation rewards. However, their risk models diverge sharply:

- LST behaves like a passively managed ETF; risk is homogenized because all protocols manage the same underlying ETH asset.

- LRT resembles a hedge‑fund structure, requiring assessment of multiple heterogeneous risks—specific AVS inflation, slashing conditions, technical bugs, etc.—and supporting diverse collateral and multi‑currency payouts.

In the ecosystem, LRT acts as an intermediary between Restakers and Operators, handling capital allocation, risk matching, and alignment with AVS security demands. Its market structure differs from the LST market (currently dominated by Lido) and requires a full‑stack ecosystem to attract capital.

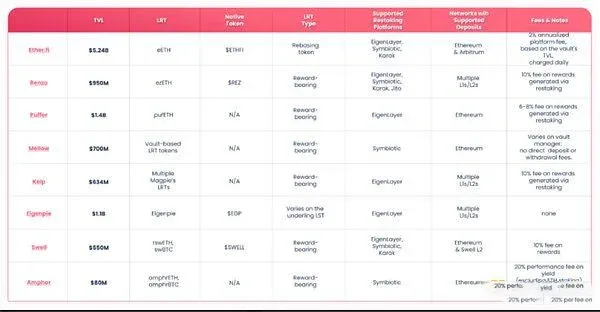

The table below lists the main differences among leading LRT projects:

(3) Restaking Platforms You Might Not Know

- Karak Network: Ranks third in TVL with roughly US $800 million, supporting LST, stablecoins, ERC‑20, LP tokens, and more as collateral. It offers customizable security layers via cross‑chain DSS (Distributed Security Service), with its L2 K2 acting as a sandbox for DSS builders.

- Exocore: Aggregates security across multiple chains in a full‑chain manner, operating as an L1 validator network that aims to reduce smart‑contract vulnerability risk.

- Nektar Network: Introduces Resilient Restaking built on the Diva stack, focusing on decentralized validation and backed by Angle Protocol and Re7 Capital.

- Verio: Launched after the Story Protocol Series B round, centering on “IP Restaking.” Users can stake IP assets to receive vIP tokens, which can then be used for extra rewards.

---

3. Bitcoin Staking and Babylon

(1) Babylon Staking Protocol Overview

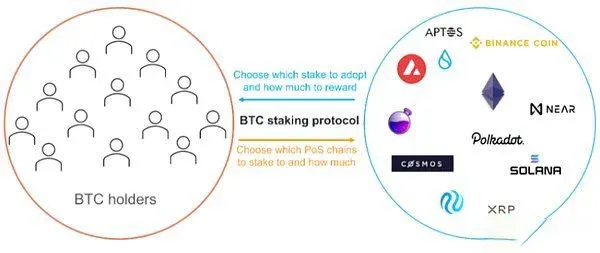

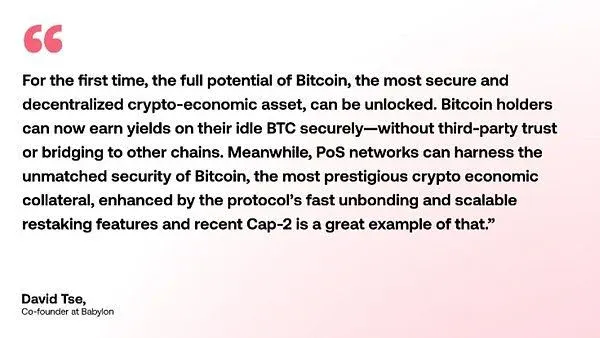

Babylon leverages shared security to use Bitcoin directly as collateral for Proof‑of‑Stake ecosystems, eliminating the need for wrapped BTC (e.g., wBTC) or other intermediary assets. The first deposit window locked 1,000 BTC, and the subsequent Cap‑2 phase attracted roughly 23,000 BTC (about US $1.6 billion) into the protocol. Babylon’s bilateral market employs timestamps, finality tools, and bond contracts to furnish security guarantees for PoS (consumer) chains and BTC holders (providers). Its modular architecture can adapt to various consensus mechanisms, allowing any chain that wishes to harness Bitcoin’s security to benefit.

Bitcoin is often called “digital gold.” Its decentralization and security are widely recognized as foundational value. Babylon expands Bitcoin’s role from pure store of value to a security provider for other networks, marking a significant milestone in the Bitcoin resurgence narrative.

(2) Bitcoin Staking Landscape

Around Babylon, several liquidity‑staking protocols are rapidly aggregating BTC assets:

- Solv: Holds over 24,000 BTC (≈ US $1.6 billion) of liquidity, serving as critical infrastructure for BTC‑Fi.

- PumpBTC: TVL has surpassed US $200 million.

- Lombard: Accumulated close to 10,000 BTC in deposits.

- Bedrock: Locks roughly US $150 million.

Beyond these, teams are developing native Bitcoin L2 solutions, DeFi protocols, wallets, and underlying infrastructure, further enriching the Bitcoin ecosystem.

- SolvBTC: Deploys across five major networks—Bitcoin, Ethereum, BNB Chain, etc.—offering cross‑chain liquidity.

- Lombard: Turns BTC from a pure store of value into a productive financial instrument for both retail and institutional users.

- PumpBTC: Provides “one‑click staking” through deep integration with Babylon.

- pSTAKE Finance: Maintains liquidity while extending BTC security to other chains.

- BabyPie: Rewards users with mBTC tokens and supports Babylon validation.

- Bedrock: A non‑custodial multi‑asset liquidity‑restaking protocol covering BTC, ETH, and IOTX.

- Chakra Network: Offers a modular settlement layer that enhances Bitcoin cross‑chain liquidity.

- Nomic: Utilizes Babylon’s stBTC to grant dual rewards on the Nomic platform.

---

4. Restaking on Solana

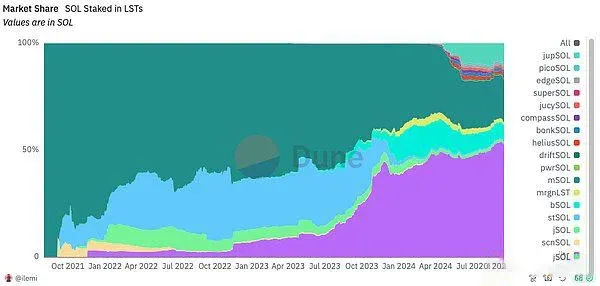

Solana achieves native staking through delegated proof‑of‑stake, amassing roughly US $50 billion of staked capital. However, liquid staking accounts for only about 8 % of that amount (versus Ethereum’s 55 %), leaving considerable upside potential. The main liquid‑staking providers are Jito and Marinade Finance, together controlling more than 70 % of the SOL LST market. Sanctum mitigates liquidity fragmentation by offering a stable‑exchange Infinity Pool.

(1) Jito

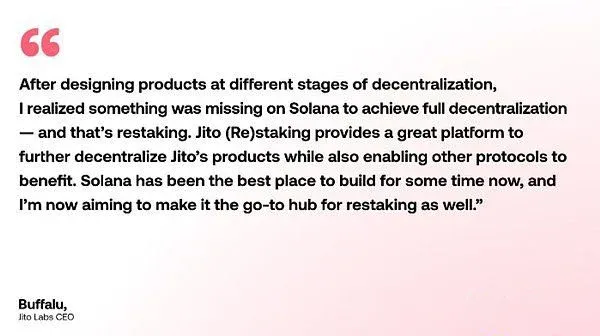

Jito is often described as Solana’s “Lido + Flashbots” hybrid. Its jitoSOL token dominates the LST market, and the team has built a custom Solana client to reduce extractable network value. In 2024, Jito launched StakeNet, an automated staking‑pool manager, and accelerated governance iterations. Its restaking solution NCN (Node Consensus Network) employs a modular architecture, issuing VRT (SPL) tokens that represent vault shares, thereby improving liquidity and composability.

Jito already enjoys a large

Related Reading

- PUMP Token Analysis: Allocation, Functionality & Solana Risks

- Crypto Cloud Mining: Mine Bitcoin Without Hardware

- Liquid Staking Leaders in Babylon: TVL Survey of 8 Protocols

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.