What Will Public Blockchains and the Tokenization Revolution Bring to Digital Currency?

Public blockchains aggregate assets, users, and applications to create a decentralized financial network, while tokenization puts asset ownership on‑chain, enhancing liquidity and global accessibility, and fostering synergistic growth within the digital‑currency ecosystem.

Today the Bitaigen editorial team walks you through the major changes that public blockchains and the tokenization revolution are expected to deliver. Happy reading!

From both a technical and an application perspective we analyze how public blockchains integrate assets, users, and services, and how tokenization boosts asset liquidity and cross‑border accessibility. The article outlines the key pathways of transformation, helping readers grasp the next wave of coordinated upgrades in the digital‑currency ecosystem—definitely worth a close read.

Summary

- Tokenization of Asset Ownership: Recording asset ownership on a blockchain enables more efficient settlement and interaction with smart contracts.

- Source of Efficiency Gains: Modern financial systems are already highly mature; tokenization alone does not instantly make everything faster. Its core value lies in unifying users, assets, and applications on a single global public platform.

- Potential at the Platform Layer: From a crypto‑market standpoint, protocols that can provide a universal global platform have the greatest upside. Grayscale’s research currently points to Ethereum as the blockchain most likely to assume this role.

What Is a Public Blockchain?

A public blockchain is a permission‑less, open‑source foundational technology that can support a wide range of use cases such as payments, gaming, digital identity, and more. Its value stems from gathering diverse applications onto a single platform; when users, capital, and apps converge, the entire ecosystem enjoys network‑effect‑driven synergies.

What Is Tokenization?

Tokenization is one of the flagship applications of public blockchains. For traditionally cumbersome asset‑management processes, moving the asset onto a blockchain can instantly raise efficiency; for most assets (aside from publicly listed equities), the benefit is primarily the network effect—delivering stronger functionality, lower costs, and broader access on a unified platform.

From a market perspective, protocols that can simultaneously host tokenized assets, investors, and related applications are the most promising. Grayscale still regards Ethereum as the leading candidate for this universal role.

History of Token Development

The evolution of tokens can be divided into three distinct phases:

| Phase | Key Characteristics | Representative Projects |

|---|---|---|

| **Blockchain 1.0** | Digital currencies exemplified by **Bitcoin (BTC)**, focused on investment returns | BTC |

| **Blockchain 2.0** | Introduction of **smart contracts**, spawning DApp development | Ethereum |

| **Blockchain 3.0** | Rise of token economies, assets moving on‑chain and extending into the real economy | ABC asset tokens, etc. |

Relationship Between Tokens and Blockchains

Tokens and blockchains are independent yet complementary components:

- Trust Foundation: Blockchains provide an immutable cryptographic base that secures token rights.

- Liquidity: Blockchains inherently enable fast, low‑cost transactions, satisfying the high‑liquidity demand of tokens.

- Decentralization: Human interference is minimized, enhancing the credibility of asset records.

- Programmability: Smart contracts endow tokens with dynamic functions such as conditional transfers, collateralization, and more.

Systemic Upgrades

As blockchain adoption widens, the issuance and tracking of securities and other physical assets could be fully executed on‑chain. Today, the beneficial ownership of many such assets is still recorded in traditional off‑chain ledgers (electronic accounts). Tokenization centers on moving that ownership to the blockchain, allowing the token price to track the underlying asset tightly.

Primary Advantages of Putting Assets On‑Chain:

- Settlement Efficiency: Near‑instant settlement, programmable payment conditions, and reduced settlement‑failure risk.

- Programmability: Supports complex business logic such as conditional transfers and compliance approvals.

- Global Accessibility: Removes geographic barriers, giving investors access to worldwide capital markets and lowering entry thresholds through fractionalization.

- Cost Reduction: Automation and the removal of intermediaries can cut underwriting fees and interest rates.

The Bank for International Settlements (BIS) introduced a tokenization “continuum” that classifies assets into those requiring extensive manual processes (e.g., real estate) and those already supported by efficient electronic ledgers (e.g., publicly traded equities). Assets that sit in the middle—such as government bonds and structured products—are often the most suitable for tokenization.

Current State and Future Outlook of Tokenization

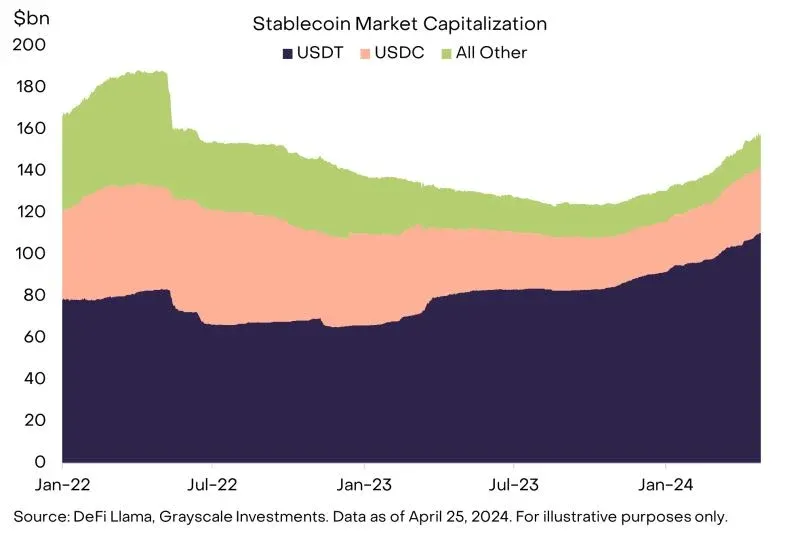

Stablecoins: The First Successful Tokenization Example

- Market capitalization has surpassed $158 billion, led by USDT and USDC.

- By holding fiat off‑chain and issuing corresponding on‑chain tokens, they enable near‑instant settlement, low‑cost payments, and seamless smart‑contract interaction.

Gold Tokens

- Representative projects XAUt (Tether Gold) and PAXG, together holding roughly $1 billion in market value.

- Provide asset‑transfer capabilities outside traditional trading hours; they exhibited noticeable volatility during recent Middle‑East tensions.

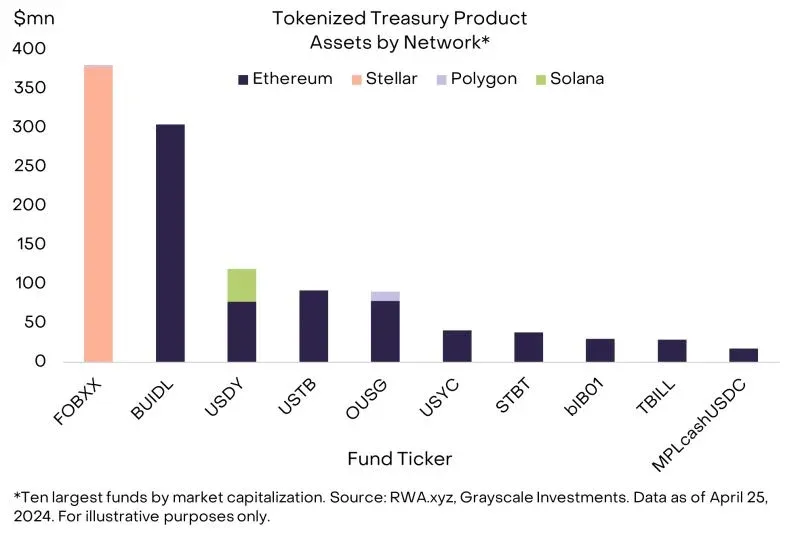

Government Bonds and Yield‑Generating Tokens

- Data from RWA.xyz shows a weighted‑average maturity of less than two years, positioning these tokens as cash equivalents.

- The market size has already exceeded $1 billion, with flagship products including FOBXX (Franklin On‑Chain US Government Money Market Fund) and BUIDL (Blackstone USD Institutional Digital Liquidity Fund).

- Approximately 60 % of the asset‑management volume resides on Ethereum, 30 % on Stellar, with the remainder spread across other chains.

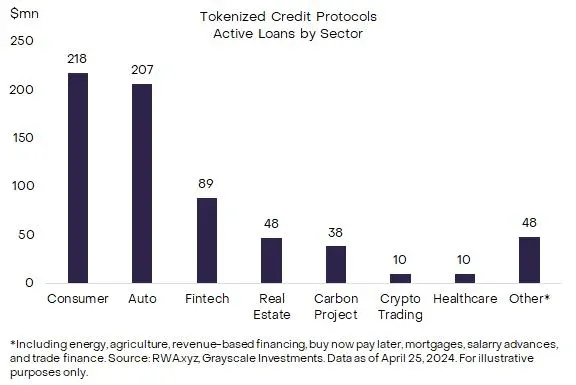

Credit Tokenization

- Encompasses consumer loans, structured credit pools (ABS, CLO), and industry‑specific financing.

- Roughly $61.2 billion of loans are currently operating on‑chain, with an average yield of about 10 %.

Other Practices

- RealT: Provides fractional ownership of U.S. real‑estate to non‑U.S. investors, locking in roughly $10.3 million of value.

- Tokenization experiments in private‑equity funds are exploring broader investor channels.

- Public‑sector entities such as the European Investment Bank and private companies like Siemens have already issued fixed‑income securities directly on‑chain.

- Tokenization of equity securities remains constrained by regulatory uncertainty and will require clearer policy guidance.

If tokenization continues to expand, on‑chain activity and fee revenue could increase dramatically. The U.S. Treasury market alone is around $26 trillion, and non‑financial sector loans total roughly $36 trillion; today, on‑chain assets represent only a tiny fraction of that total. Achieving scale will require efficient bridges to traditional brokerage and banking accounts (including SEPA and SWIFT for fiat transfers) or compelling incentives that persuade asset owners to migrate onto the blockchain.

Tax Note: In many jurisdictions, gains realized from the sale or exchange of tokenized assets may be subject to capital‑gain taxation. Users should consult local tax professionals to ensure compliance.

The Revolution Will Not Be Privatized

A common misconception is that tokenization can only happen on private, permissioned chains because regulators prevent banks from using public blockchains directly. In reality, asset‑management firms have already built solutions on public blockchains or in hybrid public‑plus‑private environments. To date, every successful tokenization case—stablecoins, government bonds, credit products—has been built on public blockchains, because the end‑users already reside on those platforms.

We anticipate that moving assets on‑chain will improve operational efficiency, but the greater value will come from seamless global connections between assets and investors, as well as interoperable application ecosystems. Public blockchains, thanks to their openness and neutrality, will remain the preferred venue for asset issuers and open‑finance developers. By contrast, private permissioned chains struggle to provide an equally neutral, worldwide network.

Trading, Fees, and Value Accumulation

Transaction fees generated by blockchain activity can be returned—directly or indirectly—to token holders in the form of dividends, buy‑backs, or other reward mechanisms. If tokenization drives higher trading volumes, those fees can accumulate onto the associated token. The exact mechanism depends on the protocol’s design and token characteristics (see Figure 5).

*Figure 5: Value Flow for Tokenized Assets*

Within smart‑contract platforms, Layer 1 (and, in the future, Layer 2) serves as the global public layer for tokenized assets. Their native tokens are used to pay gas, earn staking rewards, or gain value through built‑in deflationary mechanisms.

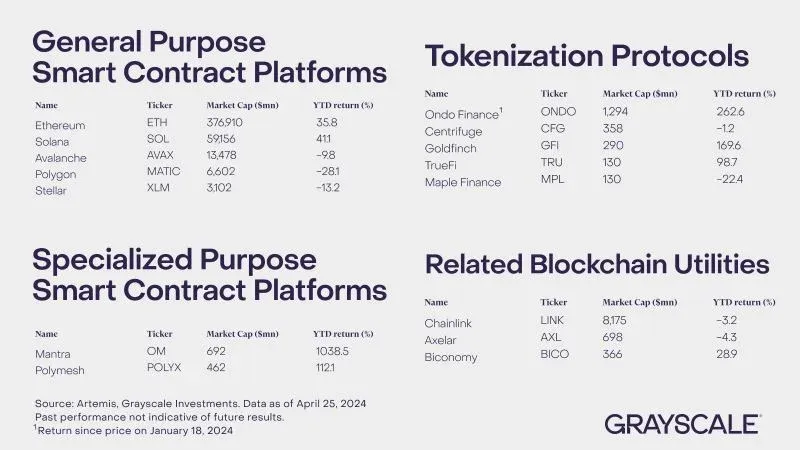

Although competition among chains is fierce, Ethereum still leads in terms of users, locked value, and decentralized application (dApp) activity, and it offers sufficient decentralization and neutrality to satisfy the requirements of a global tokenization platform. Other chains that may benefit include Avalanche, Polygon, Stellar, as well as purpose‑built tokenization networks such as Mantra and Polymesh.

Close behind are the tokenization protocols that provide the tooling for asset onboarding (e.g., Ondo Finance, Centrifuge). Some of these protocols issue governance tokens, while others do not. When evaluating such tokens, investors should examine the project's governance framework and its commitment to sharing protocol revenue.

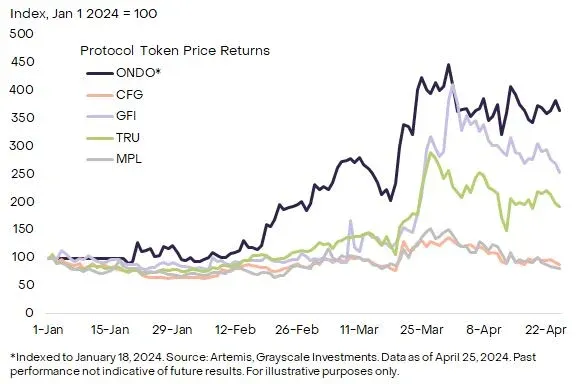

*Figure 6: Annual Returns of Some Tokenization Protocols*

In addition, growth in on‑chain activity fuels the development of complementary infrastructure. For instance, Chainlink is advancing its cross‑chain interoperability protocol (CCIP) to become the core messaging layer across blockchains, while Biconomy offers a “paymaster” service that lets users pay gas with non‑native tokens. Both belong to the “public utilities and crypto services” sector identified by Grayscale.

Outlook for Tokenization

Grayscale believes that digital commerce is shifting from closed, centrally‑mediated platforms to open, decentralized ecosystems built on public blockchains. Tokenization, as a key driver of blockchain adoption, could become a pivotal catalyst given the massive scale of global capital markets. If public blockchains can bring together borrowers and lenders (or asset issuers and investors) while reducing the role of existing fintech intermediaries, the resulting surge in network activity may lift the intrinsic value of native blockchain tokens.

The above constitutes the Bitaigen editorial team’s in‑depth analysis of what public blockchains and the tokenization revolution will bring to digital currency. We hope it helps you gain a deeper understanding of this transformative trend.

Related Reading

- Public Blockchain for Digital Currency: Core Concepts, Consensus Mechanisms & Ec

- Public vs Private Blockchains: Key Differences and Consortium hybrids

- RWA Tokens Explained: Value, Transparency & Liquidity

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.