In this article we systematically outline the core concepts of Web 3 payments, the structure of its ecosystem, and the differences compared with traditional payments. We also select key projects within the sector for deep analysis. By reviewing the regulatory environment and future trends, readers can grasp the industry’s trajectory, uncover potential opportunities, and look forward to richer case studies and insights in later sections—material worth a careful read.

Introduction

As blockchain technology matures, payment methods based on crypto assets are gradually infiltrating the traditional financial system. This paper examines the concept of Web 3 payments, their advantages over legacy payment rails, the ecosystem architecture, the regulatory landscape, and the flagship projects operating in the space. It also offers a forward‑looking view of possible development paths, helping readers to obtain a comprehensive picture of this emerging track.

6. Future Outlook

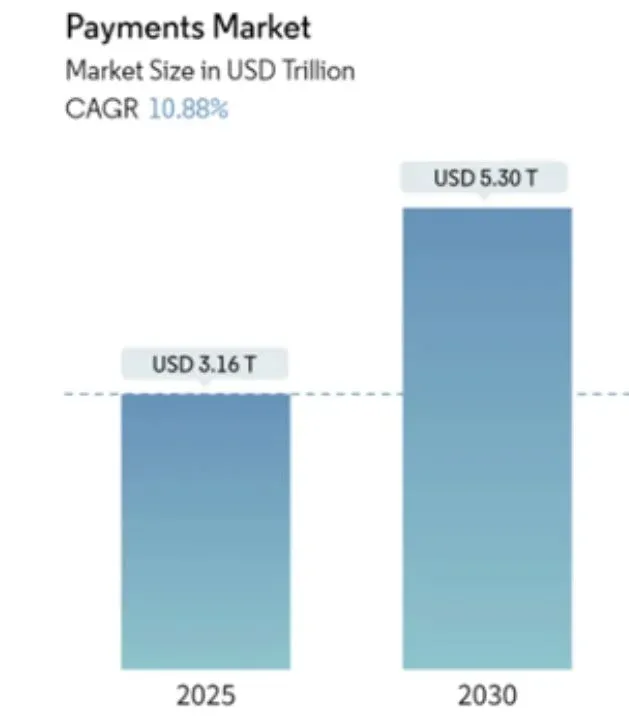

The traditional payments industry processes an enormous volume of transactions—about 34 trillion payments worldwide in 2023, with a total value of roughly $1.8 trillion and annual revenue of about $2.4 trillion. Forecasts suggest revenue will exceed $3.2 trillion by 2025 and could reach $5.3 trillion by 2030, implying a compound annual growth rate (CAGR) of approximately 10.9 %. By contrast, global stable‑coin transaction volume in 2023 was around $3 trillion, representing a market penetration of less than 0.2 %. If Web 3 payments were to capture a modest 10 % share of the overall payments market, the addressable size could surpass $300 billion.

Drawing on the paths taken by fintech giants such as Alipay and WeChat Pay to win share from traditional banking, PayFi (payment‑focused finance) and SocialFi (social‑focused finance) are poised to become the driving forces that accelerate mainstream adoption of Web 3 payments.

6.1 PayFi: Deep Integration of Payments and DeFi

PayFi aims to fuse payment functionality with decentralized finance (DeFi) services, delivering a full‑stack financial experience that spans payments, lending, savings, and asset management. When a user completes a payment, a portion of the funds can be automatically routed into yield farms or other investment products, turning every transaction into a value‑adding event. As the model matures, payment use‑cases may expand into insurance, bonds, and other traditional financial products, attracting more banks, fintechs, and DeFi protocols into the ecosystem.

6.2 SocialFi: Value Flow Within Social Ecosystems

SocialFi embeds payment capabilities directly into social platforms and the creator economy, leveraging decentralized payment protocols to enable instant value exchange between content creators and community members. Take X Pay (formerly Twitter Pay) as an example: the project integrates crypto micro‑payments, allowing users to tip, pay for premium content, or otherwise transact directly within social interactions, thereby providing a fresh engine for platform monetisation.

1. What Is Web 3 Payment?

Web 3 payment refers to a novel payment paradigm built on blockchain and crypto‑assets. By operating on a decentralized network, it removes many traditional intermediaries, offering a low‑threshold, low‑cost, and highly efficient transaction experience.

- Blockchain network: Relies on a public, immutable distributed ledger and smart contracts that automatically execute payment instructions, eliminating manual review and reconciliation steps while boosting accuracy and security.

- Crypto‑asset medium: Most use‑cases employ fiat‑pegged stablecoins (e.g., USDT, USDC) to avoid the price volatility associated with assets like Bitcoin, making them especially suitable for cross‑border transfers.

Tax note: Gains or losses arising from crypto‑asset transactions may be taxable under the tax laws of the user’s jurisdiction. Participants should consult local tax professionals to ensure compliance.

2. Advantages of Web 3 Payments Over Traditional Payments

Legacy payment systems typically involve banks, payment gateways, clearing houses, and other layers of intermediaries, leading to several pain points:

- Financial exclusion: Users without a bank account or formal identity verification struggle to access the global financial network.

- Fees and latency: Every intermediate charges a fee, and cross‑border remittances often take several days to settle.

- Bankruptcy risk: Credit risk of intermediaries can be indirectly transferred to end‑users.

The following three common cross‑border payment pathways illustrate Web 3’s competitive edge.

2.1 Bank‑to‑Bank Payments

Process: Originating bank → SWIFT → multiple correspondent banks → destination‑country clearing system → destination bank

Cost & Speed: Fees are relatively high and lack transparency; settlements can take several days, with hidden charges sometimes appearing en route.

2.2 Third‑Party Payment Providers

Process: Sender’s bank → third‑party payment platform → (optional) currency conversion → receiver’s bank

Cost & Speed: Fee structures are more predictable, platforms publish their rates, and settlement can range from instant to a few business days.

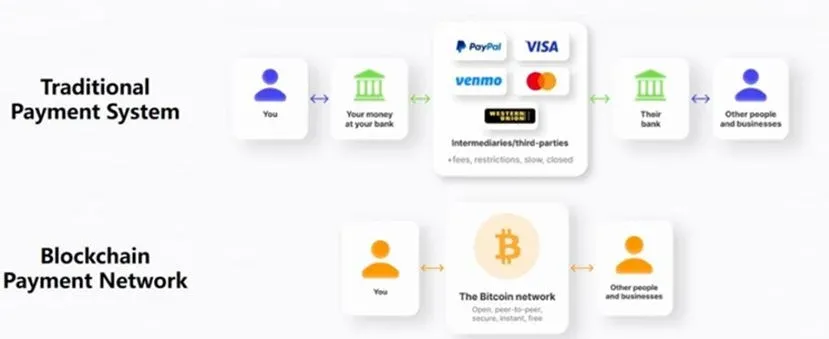

2.3 Web 3 Payments

Process: Sender’s wallet → smart‑contract execution → blockchain network validation → receiver’s wallet

Cost & Speed: The primary cost is the on‑chain gas fee, which is generally low and fully auditable; confirmation time depends on the chosen chain’s performance and is often within minutes.

Figure 1: Comparison of Traditional Payment Flow vs. Web 3 Payment Flow

Evaluated across inclusivity, cost, efficiency, and transparency, Web 3 payments consistently outperform the legacy alternatives:

- Financial inclusion: Anyone with an internet connection can transact using crypto assets, dramatically lowering entry barriers.

- Low fees: By stripping out banks and clearing houses, the only expense is the blockchain gas fee; cross‑border exchange spreads are virtually zero.

- Speed: Peer‑to‑peer settlement on a decentralized network dramatically reduces settlement time, especially for large or cross‑border amounts.

- Transparency & traceability: All transaction data is publicly recorded on‑chain, facilitating audits, regulatory oversight, and fraud prevention.

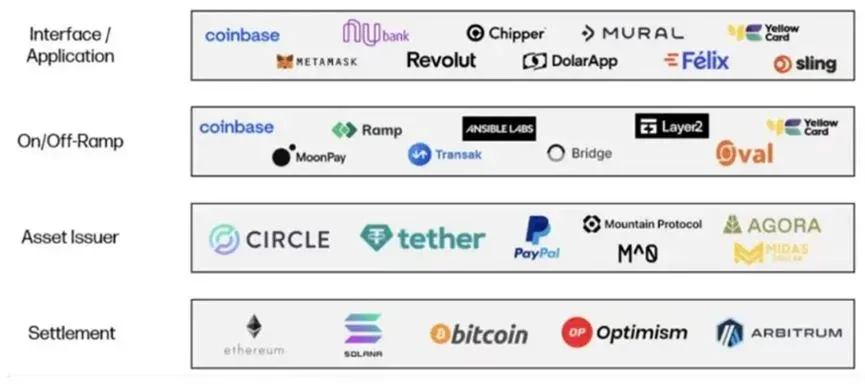

3. Ecosystem and Business Models

3.1 Ecosystem Structure

Core participants in the Web 3 payment sector can be grouped into four categories:

- Stable‑coin issuers – e.g., Tether (USDT) and Circle (USDC), which provide digitally anchored value.

- Public blockchains – Ethereum, Solana, and others that supply the underlying ledger and smart‑contract execution environment, replacing centralized clearing networks.

- On‑ and off‑ramps – entities that handle fiat‑to‑crypto and crypto‑to‑fiat conversions and provide liquidity.

- Payment platforms – including decentralized wallets and centralized exchanges that offer merchants and users the payment interface and settlement layer.

Figure 2: Web 3 Payment Ecosystem Diagram

3.2 Business Models

- Asset issuers: Earn returns on the fiat reserves that back their stablecoins, typically through low‑risk investments.

- Public blockchains: Generate revenue primarily from network usage fees (gas).

- On/Off‑ramps: Charge a conversion fee for fiat↔crypto swaps, with industry‑average rates hovering around 0.6 % of transaction value.

- Payment platforms: Monetise via integration fees (APIs, plugins), currency conversion spreads, and rewards earned from user‑provided liquidity or staking.

Because on/off‑ramp fees and integration services benefit from strong network effects, they tend to scale exponentially with user growth and transaction volume, reinforcing competitive moats for established platforms.

4. Regulatory Compliance

Regulatory attitudes toward Web 3 payments vary worldwide, but most jurisdictions are moving toward licensing frameworks that enforce anti‑money‑laundering (AML) and know‑your‑customer (KYC) requirements. Below are the key points for major jurisdictions.

4.1 United States

- Regulator: FinCEN (Financial Crimes Enforcement Network), a bureau of the Treasury Department, oversees AML and counter‑terrorist financing.

- Legal basis: The Bank Secrecy Act (BSA) expands the definition of “money transmission” to include crypto‑assets, obligating businesses to obtain a Money Services Business (MSB) licence.

- Critical licences: New York’s BitLicense is widely regarded as the “golden ticket” for U.S. market entry; each state also requires its own Money Transmission Licence (MTL).

4.2 European Union

- Regulatory framework: The Markets in Crypto‑Assets Regulation (MiCA) is gradually harmonising rules across member states.

- Service providers: Under MiCA, firms offering crypto‑asset services must register as Virtual Asset Service Providers (VASPs).

- Examples: Coinbase, MoonPay and others have secured Electronic Money Institution (EMI) licences in the UK and Ireland and are awaiting full MiCA rollout to operate uniformly across the 27‑country bloc.

4.3 Hong Kong

- Supervisors: Securities and Futures Commission (SFC) together with the Hong Kong Monetary Authority (HKMA).

- Requirements: All crypto‑asset exchanges and related service providers operating in Hong Kong must hold a VASP licence and, where applicable, a Trust or Custody Service Provider (TCSP) licence for client‑asset custody.

4.4 Singapore

- Regulator: Monetary Authority of Singapore (MAS) governs digital payment tokens (DPT) under the Payment Services Act.

- Licence regime: Companies offering DPT services must obtain a DPT licence; MAS grants a limited exemption period for qualifying startups before full licensing is required.

- Industry snapshot: Circle, Paxos, Coinbase and others have already secured the licence, allowing lawful entry into the Asian market.

4.5 Dubai

- Authority: Virtual Assets Regulatory Authority (VARA) oversees crypto‑asset activities across the emirate.

- Policy stance: While adhering to international compliance standards, VARA offers a relatively permissive entry environment, attracting numerous Web 3 payment projects.

4.6 Japan

- Regulator: Financial Services Agency (FSA) conducts rigorous examinations of crypto exchanges and wallet services.

- Mandatory licence: Operators must obtain a Virtual Currency Exchange Licence (VFA) and comply with AML/KYC obligations.

- Trend: The government is exploring integration of crypto assets with a prospective Central Bank Digital Currency (CBDC).

4.7 South Korea

- Supervisors: Financial Services Commission (FSC) and Financial Supervisory Service (FSS).

- Compliance: All entities facilitating crypto‑asset trading must secure a VASP licence and submit AML reports.

5. Highlighted Projects

5.1 Coinbase Pay: Bridging Trading and Payments

Coinbase offers Coinbase Pay, a one‑stop crypto payment solution for merchants and consumers. The service supports Bitcoin, Ethereum, USDC and other assets, and allows merchants to instantly convert receipts into fiat (USD) to hedge against price volatility.

- Merchant integration: Built on the Coinbase Commerce API, merchants can accept crypto payments without managing a wallet themselves, achieving end‑to‑end connectivity.

- Compliance footprint: Leveraging licences obtained in the United States, United Kingdom, Ireland and Singapore, Coinbase can legally provide fiat↔crypto conversion services.

- Cross‑border advantage: By utilising stablecoins such as USDC, Coinbase enables low‑cost, near‑real‑time settlement for international trade.

5.2 PayPal: A Traditional Payments Giant Tests Web 3

In 2023 PayPal launched its own stablecoin, PayPal USD (PYUSD), marking its formal entry into Web 3 payments.

- PYUSD features: Pegged 1:1 to the U.S. dollar, users can purchase, hold, and transfer PYUSD directly within their PayPal accounts.

- Compliance safeguards: PYUSD is custodial‑backed by Paxos; all transactions undergo AML and KYC checks to satisfy regulatory expectations in the United States, the EU and major Asian markets.

- Wallet ecosystem: Through the PayPal Crypto Hub, users can seamlessly swap between crypto assets and fiat, creating a frictionless bridge between Web 3 and legacy payments.

5.3 MetaMask: Expanding Payment Capabilities for a Decentralised Wallet

MetaMask leverages its massive user base to continuously enhance payment functionality.

- Portfolio & swap tools: Users can instantly exchange fiat‑linked stablecoins for crypto and push funds directly to bank accounts.

- Third‑party integrations: Partnerships with MoonPay, Transak and similar providers give MetaMask users a variety of on‑ramp and off‑ramp options, including credit/debit cards and SEPA/SWIFT bank transfers.

- Snaps plug‑in architecture: The latest Snaps release enables developers to add support for non‑EVM chains (e.g., Solana, Aptos, Cosmos), widening cross‑chain payment scenarios.

- Super‑wallet vision: By aggregating payments, asset management, and cross‑chain bridging, MetaMask is building a “one‑stop” payment gateway for the entire multi‑chain ecosystem.

Summary

- Concept recap: Web 3 payments harness blockchain and stablecoins to deliver a disintermediated, low‑cost, high‑efficiency payment model.

- Ecosystem participants: Stable‑coin issuers, public blockchains, fiat↔crypto on/off‑ramps and payment platforms each have distinct revenue streams—reserve‑investment yields, gas fees, conversion commissions and integration fees respectively.

- Regulatory trajectory: Major financial hubs are introducing licence regimes and VASP registration requirements to bring Web 3 payments under AML/KYC oversight, ensuring growth within a safe, transparent framework.

- Industry outlook: Innovative constructs such as PayFi and SocialFi are injecting fresh momentum into Web 3 payments; if a 10 % market penetration is achieved, the addressable market could exceed $300 billion.

This concludes the full analysis of “What Is Web 3 Payment? Key Projects in the Web 3 Payment Track and Future Outlook.” For deeper dives into Web 3 payment topics, continue following Bitaigen’s historical articles or explore the related links below. Thank you for your ongoing support!

Related Reading

- Liquidity Mining vs Staking: Key Differences, Rewards & Risks

- Crypto Prediction Markets: Benefits & How They Work

- 2025 Crypto Launchpad Landscape: Web3 IDO, LBP & Funding

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.