In many cryptocurrency investment products you will often see APR or APY displayed. What exactly do these terms represent? Can you simply multiply the amount you invest by the shown number to obtain your earnings?

This article will explain the meaning of APR and APY, highlight the differences between them, and show you how to calculate the potential returns using APR and APY. Keep in mind that most crypto exchanges quote floating APR/APY rates, not guaranteed returns, so actual earnings may differ from the calculated figures. For illustration purposes this article uses fixed‑rate examples, but you should always consider current market conditions when applying the formulas.

The Bitaigen editorial team reminds readers that the real meanings of APR and APY in investment products are frequently misunderstood. Starting from the concepts, we dissect the fundamental calculation differences and provide practical steps for estimating returns, helping you evaluate potential rewards more accurately in the volatile crypto environment. If you want to master the correct formulas and avoid common pitfalls, keep reading.

What Is the Annual Percentage Rate (APR)?

Annual Percentage Rate, abbreviated APR, represents the percentage of interest earned on the principal over a one‑year period, calculated using simple interest. In traditional finance, APR is commonly used for bank deposits and loan products. For borrowers, APR reflects the cost of borrowing; for depositors, it indicates the earnings on a deposit.

How APR Is Calculated

The formula is straightforward; let’s start with a everyday example:

- You deposit $100 in a bank that offers a 6 % annual rate. If the rate stays constant for the whole year, your account balance after one year will be $106, where $100 is the principal and $6 is the interest.

- Another depositor also puts in $100, but withdraws after six months. Because the money was only on deposit for half a year, they receive $103, with $3 representing six‑month interest.

From these scenarios we derive the following equations:

- Total deposit = Principal + Interest

- Interest = Principal × Rate × Time

Interest = Principal × Interest Rate × Time

Substituting the second equation into the first gives:

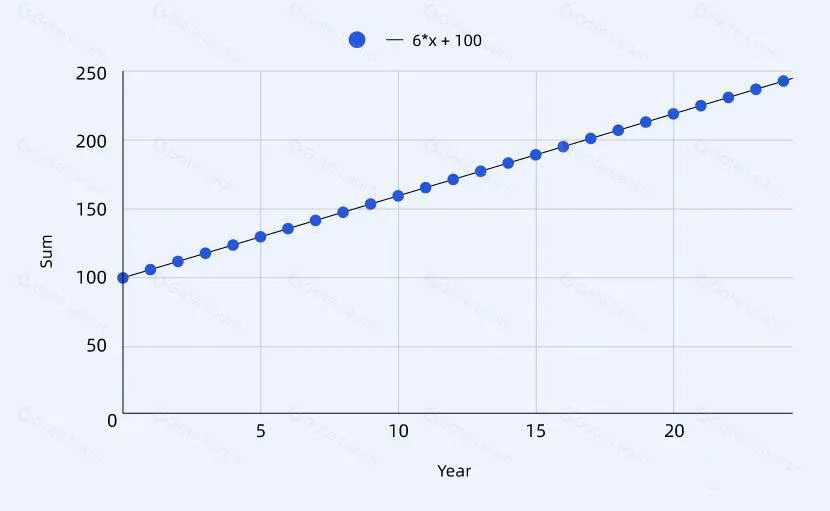

- Total deposit = Principal × (1 + Rate × Time)

Sum = Principal × (1 + Interest Rate × Time)

Here Time is expressed in years, and the annual rate quoted by the bank is the APR. Because APR uses simple interest, the accumulated amount grows linearly with time, appearing as a straight line on a graph whose slope equals the APR.

What Is the Annual Percentage Yield (APY)?

Annual Percentage Yield, abbreviated APY, also measures the percentage of interest earned on the principal over a year, but it is calculated using compound interest. APY not only accounts for interest generated on the original principal, it also reinvests that interest to produce additional earnings.

How APY Is Calculated

Again, using a deposit example:

- You deposit $100 at a 6 % annual rate. After one year the balance is $106 (the same as with APR).

- If you keep the $106 deposited for a second year, the interest for that year becomes $106 × 6 % = $6.36, and the final balance after two years is $112.36.

From this we can see:

- Compound interest causes the effective principal to increase each period.

- With the same nominal rate, compound interest yields more interest than simple interest.

The generic compound‑interest formula is:

- Total deposit = Principal × (1 + Rate) ^ Number of Compounding Periods

Sum = Principal × (1 + Interest Rate) ^ Number of Compounds

If compounding occurs once per year, APR and APY are numerically identical. However, increasing the compounding frequency changes the result. For example, a 6 % nominal rate compounded semi‑annually (twice per year) yields after one year:

100 × (1 + 0.06 / 2) ^ 2 = $106.09

Thus we obtain:

- Total deposit = Principal × (1 + Rate / Compounding Frequency) ^ Compounding Frequency

Sum = Principal × (1 + Interest Rate/Compound Frequency) ^ Compound Frequency

The relationship between interest and principal can also be expressed as:

- Interest = Total deposit – Principal = Principal × APY

From which the APY expression follows:

- APY = (1 + Rate / Compounding Frequency) ^ Compounding Frequency – 1

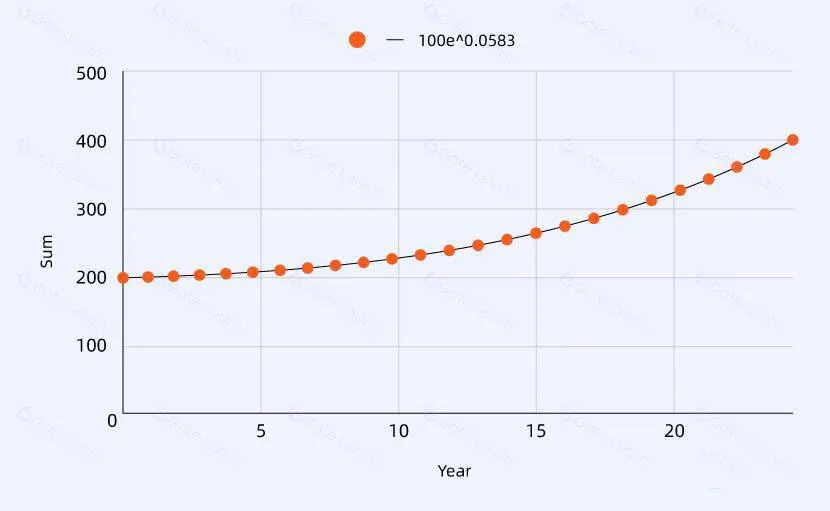

APY grows as either the nominal Rate or the Compounding Frequency increase, but the marginal benefit of higher frequency diminishes. When the compounding frequency approaches infinity (continuous compounding), APY can be approximated by:

APY ≈ e ^ Rate – 1

where e is the base of natural logarithms, approximately 2.71828.

Why Distinguish Between APR and APY?

| Name | Calculation Method | Typical Use Cases |

|------|--------------------|-------------------|

| APR | Simple interest | Loans, straightforward yield products |

| APY | Compound interest | Yield‑generating investments, products where reinvestment matters |

The purpose of distinguishing the two is to show the yield gap between simple and compound interest, helping investors select the appropriate formula. The compounding interval (daily, monthly, yearly, etc.) can dramatically affect the final return, whereas APR can be obtained with a simple multiplication or division.

How to Compute APR and APY? Do the Math Yourself

APR formula

\[

\text{APR} = \frac{\text{Annual Earnings}}{\text{Principal Invested}} \times 100\%

\]

If the earnings cover less than a full year, multiply by \(\frac{365}{\text{Number of Earned Days}}\) to annualise.

APY formula (more involved)

\[

\text{APY} = \left[ \left( \frac{\text{Principal + Earnings}}{\text{Principal}} \right)^{\frac{\text{Investment Period}}{\text{Yield Calculation Frequency}}} \right]^{\frac{1}{\text{Yield Calculation Frequency}}} - 1 \times 100\%

\]

Here “Investment Period” is expressed in years.

If you only need a quick estimate of one‑year earnings, you can use:

- APR: Earnings = Principal × APR

- APY: Earnings = Principal × APY

For multi‑year cumulative earnings:

- APR: Total earnings = Principal × APR × Number of Years

- APY: Total earnings = Principal × (1 + APY)^{Number of Years} – Principal

Example: With a 10 % APR, investing $10,000 yields after five years

\(10{,}000 \times 10\% \times 5 = $5,000\).

If the APY is also 10 %, the five‑year earnings become

\(10{,}000 \times (1+10\%)^{5} - 10{,}000 = $6,105\).

APR is easy to compute mentally; APY involves exponentiation, so using a calculator or an online tool is advisable.

How to Earn More With the Same APR or APY?

Earnings depend on principal, rate (APR/APY), and holding period. Consequently:

- Invest a larger principal → Earnings scale proportionally.

- Extend the holding period → Earnings accumulate over time (especially with APY).

For instance, a product offering 5 % APR gives a $500 return on a $10,000 deposit after one year. Investing $100,000 under the same terms would generate $5,000 in one year—a ten‑fold increase. Likewise, with a $10,000 principal, a one‑year holding period yields $500, whereas a five‑year period yields $2,500.

A few cautions:

- Products touting extremely high APRs (e.g., monthly returns above 10 %) usually carry high risk and may be scams.

- Crypto‑based APR/APY rates fluctuate with market conditions; strong market phases produce higher yields, while bear markets reduce them. Do not chase short‑term high rates without due diligence.

- Even an astronomically high APR can be offset by price volatility of the underlying asset. For example, a token may display a 1,000 % APR, but if its price drops 99 % within the year, the net asset value shrinks dramatically.

Tax note: Crypto earnings, including those derived from APR/APY products, may be taxable in your jurisdiction. Consult a tax professional to understand your local obligations.

Where Can You View APR and APY? Binance as an Example

Most platforms display the APR or APY directly on the purchase page of each investment product.

On Binance’s main investment page (official download: https://www.bitaigen.com/binance/download / official registration: https://www.bitaigen.com/binance), you can see the APR associated with each coin. US residents should use Binance.US, not the global Binance platform. When reviewing the rates, keep in mind:

- Rates may change: They adjust automatically with market movements, so the actual return may differ from the displayed figure.

- Tiered rates: Some products offer higher rates up to a certain amount, with lower rates applied to any excess.

For example, the “Earn USDT” product shows a 6.61 % APR that applies only to the first 200 USDT of your deposit. Any amount above that (e.g., the next 300 USDT) is credited at 1.61 %. If you deposit 500 USDT, the first 200 USDT earn at 6.61 % while the remaining 300 USDT earn at 1.61 %.

Frequently Asked Questions About APR and APY

If two products have identical APR and APY, which should I choose?

Assuming all other risk factors are equal, the product that compounds (i.e., offers APY) will generally deliver a higher return, making the APY option the more attractive choice.

That concludes the comprehensive guide to “What are APR and APY in the crypto world? What are the differences? How can you calculate your potential earnings?” For more related articles, follow Bitaigen.

💡 Register on Binance with referral code B2345 for the maximum trading fee discount. See Binance complete guide.